Tax Penalty Cancelled: Court Upholds Tribunal's Decision in Favor of Assessee

Full News

Tax Penalty Cancelled: Court Upholds Tribunal's Decision in Favor of Assessee

Tax Penalty Cancelled: Court Upholds Tribunal's Decision in Favor of Assessee

This case involves an appeal by the revenue department against a decision by the Income Tax Appellate Tribunal (ITAT) that upheld the cancellation of a penalty imposed on Torque Pharmaceuticals P. Ltd. The High Court dismissed the appeal, agreeing that the penalty was correctly cancelled as there was no evidence of malafide intent or inaccurate income reporting by the assessee.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax Vs Torque Pharmaceuticals P. Ltd. (High Court of Punjab & Haryana)

ITA No.417 of 2015 (O&M)

Date: 16th March 2016

Key Takeaways:

1. Mere disallowance of expenditure doesn't automatically imply concealment of income or furnishing inaccurate particulars.

2. For penalty under Section 271(1)(c) (of Income Tax Act, 1961), there must be clear evidence of concealment or inaccurate reporting.

3. Bonafide claims, even if not accepted by revenue authorities, don't necessarily lead to penalties.

Issue:

Was the Income Tax Appellate Tribunal (ITAT) correct in upholding the decision of the Commissioner of Income Tax (Appeals) [CIT(A)] to delete the penalty levied for the assessment year 2006-07?

Facts:

1. Torque Pharmaceuticals P. Ltd. filed a nil income tax return on 4.12.2006 for the assessment year 2006-07.

2. The case was selected for scrutiny and assessed under section 143(3) (of Income Tax Act, 1961) on 19.12.2008.

3. The Assessing Officer made several additions and initiated penalty proceedings.

4. The assessee appealed to the CIT(A), which was partly allowed on 31.5.2010.

5. The assessee then appealed to the ITAT, which partly allowed the appeal on 4.7.2011.

6. The Assessing Officer imposed a penalty of ₹22,88,770/- under Section 271(1)(c) (of Income Tax Act, 1961) on 29.3.2012.

7. The CIT(A) cancelled this penalty on 1.7.2013.

8. The ITAT upheld the CIT(A)'s order on 19.5.2015.

9. The revenue department then filed this appeal to the High Court.

Arguments:

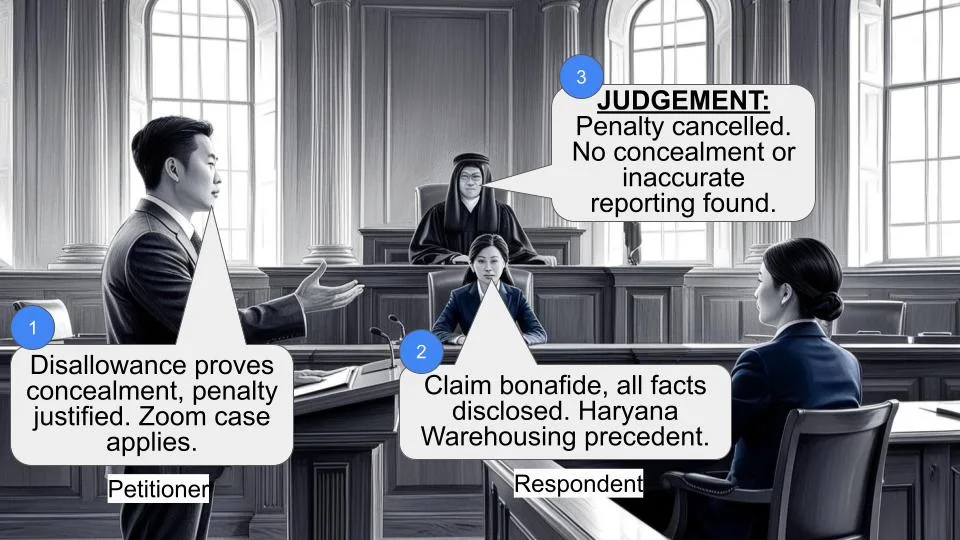

Revenue's Argument:

- The ITAT was wrong in upholding the CIT(A)'s decision to delete the penalty.

- They cited the judgment of the Delhi High Court in CIT vs. Zoom Communication (P) Limited (2010) 327 ITR 510 to support their case.

Assessee's Argument:

- The claim for deduction was bonafide and all facts were disclosed.

- There was no concealment of income or furnishing of inaccurate particulars.

- The disallowance of expenditure doesn't automatically imply concealment or inaccuracy.

Key Legal Precedents:

1. CIT vs. Haryana Warehousing Corporation 314 ITR 215: Held that a legitimate and bonafide deduction claim, even if disallowed, doesn't warrant a penalty if all facts were disclosed.

2. CIT vs. Reliance Petroproducts (P) Limited, (2010) 322 ITR 158: The Supreme Court held that for a penalty under section 271(1)(c) (of Income Tax Act, 1961), there must be concealment of income or furnishing of inaccurate particulars.

3. AT&T Communications Services (India) Pvt. Limited (42 DTR 22): This case was cited by the CIT(A) for cancelling the penalty.

Judgement:

The High Court dismissed the revenue's appeal, concluding that:

1. No finding had been recorded by lower authorities that the assessee's claim was malafide.

2. The Tribunal had examined all material and agreed with the CIT(A)'s cancellation of the penalty.

3. A bonafide claim, even if not accepted by revenue, doesn't imply concealment or inaccurate reporting of income.

4. The case cited by the revenue (Zoom Communication) was not applicable as it involved malafide intention, which wasn't present here.

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was whether a penalty should be imposed on the assessee for claiming certain deductions that were later disallowed.

2. Q: Why did the court dismiss the revenue's appeal?

A: The court found no evidence of malafide intent or inaccurate reporting by the assessee, which are necessary for imposing a penalty under Section 271(1)(c) (of Income Tax Act, 1961).

3. Q: What's the significance of this judgment for taxpayers?

A: It reinforces that bonafide claims, even if disallowed, don't automatically lead to penalties. Taxpayers can make claims they believe are legitimate without fear of automatic penalties if those claims are later rejected.

4. Q: What conditions must be met for a penalty under Section 271(1)(c) (of Income Tax Act, 1961)?

A: There must be clear evidence of either concealment of income or furnishing of inaccurate particulars of income.

5. Q: How does this case differ from the Zoom Communication case cited by the revenue?

A: In the Zoom Communication case, there was evidence of malafide intention in furnishing inaccurate particulars, which wasn't present in this case.

1. This appeal has been preferred by the revenue under section 260A (of Income Tax Act, 1961) (in short, “the Act”) against the order dated 19.5.2015, Annexure A.6 passed by the Income Tax Appellate Tribunal, Chandigarh Bench 'A' (in short, “the Tribunal”) in ITA No.972/CHD/2013, for the assessment year 2006-07, claiming following substantial question of law:-

“Whether the ITAT was right in law in upholding the decision of the CIT(A) deleting the penalty levied for assessment year 2006-07 who has relied upon the decision of ITAT Delhi in AT&T Communication Services India Pvt. Limited (42 DTR 22) and the decision relied upon by the Hon'ble ITAT is adequately countered by the judgment of the Hon'ble Delhi High Court in the case of CIT vs. Zoom Communication (P) Limited (2010) 327 ITR 510?”

2. A few facts relevant for the decision of the controversy involved as narrated in the appeal may be noticed. The assessee company filed its return of income on 4.12.2006 declaring nil income. The case was selected for scrutiny and assessed under section 143(3) (of Income Tax Act, 1961) on 19.12.2008. The Assessing Officer made following additions and initiated the penalty proceedings on all the issues:-

i) Addition of 26,96,304/- on account of non deduction of TDS on freight inward.

ii) Addition of 63,447/- on account of non deduction of TDS on freight outward.

iii) Addition on account of repair and maintenance of cars under section 40(a)(ia) (of Income Tax Act, 1961) amounting to 1,94,593/-.

iv) Addition on account of capitalization of interest amounting to 5,82,625/- plus 2053/- plus 8302/-.

v) Addition under section 40A(3) (of Income Tax Act, 1961) amounting to 18,297/-.

vi) Addition on account of disallowance under section 80IC (of Income Tax Act, 1961) on reallocation of expenses amounting to 28,63,569/-.

vii) Addition amounting to 1,42,520/- on account of interest debited to Dera Bassi unit and treated as relating to Baddi Unit.

viii) Addition of 3,70,836/- on account of claim of expenditure of interest payment which was never paid by the assessee.”

The assessee filed appeal before the Commissioner of Income Tax (Appeals) which was partly allowed vide order dated 31.5.2010, Annexure A.2. Still not satisfied, the assessee filed appeal before the Tribunal. Vide order dated 4.7.2011, Annexure A.3, the appeal was partly allowed. Thereafter, the Assessing Officer imposed penalty under Section 271(1)(c) (of Income Tax Act, 1961) on all the issues amounting to ` 22,88,770/- vide order dated 29.3.2012, Annexure A.4. The assessee filed appeal before the Commissioner of Income Tax (Appeals) [CIT(A)]. Vide order dated 1.7.2013, Annexure A.5, the CIT(A) cancelled the penalty imposed by the Assessing Officer. The revenue filed appeal before the Tribunal. Vide order dated 19.5.2015, Annexure A.6, the Tribunal upheld the order passed by the CIT(A). Hence the instant appeal by the revenue.

3. We have heard learned counsel for the revenue.

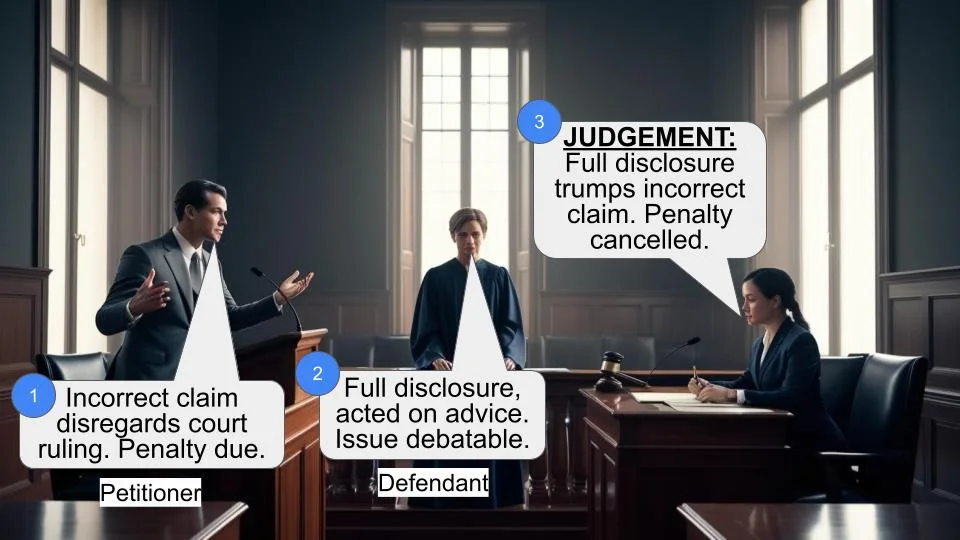

4. The primary challenge in this appeal is to the cancellation of penalty on addition made on account of disallowance of expenditure under Section 40(a)(ia) (of Income Tax Act, 1961). The assessee had made a claim of deduction in the return of income. No finding has been recorded by the authorities below that the claim made by the assessee is malafide. It has been categorically recorded by the Tribunal after examining the entire material on record that the CIT(A) had rightly cancelled the penalty against the assessee. It was further recorded that the assessee made a bonafide claim of deduction of the expenditure and even though it was not acceptable to the revenue would not lead to the conclusion that the assessee had concealed the particulars of income or filed inaccurate particulars of income. The relevant findings recorded by the Tribunal read thus:-

“8. We have considered the rival submissions and material available on record.

The issue involved in the appeal is regarding cancellation of penalty on addition made on account of disallowance of expenditure under section 40(a)(ia) (of Income Tax Act, 1961). The assessee has disclosed the entire facts before the authorities below without concealing any income. The assessee made a claim of deduction in the return of income and explained the facts but the same were not accepted by the authorities below and additions have been confirmed. Therefore, it is a case of mere disallowance of expenditure without bringing any adequate material against assessee to prove that assessee has concealed the particulars of income or has furnished inaccurate particulars of income. The appeal of the assessee on substantial question of law with regard to disallowance under the provision had been admitted by Hon'ble Punjab and Haryana High Court. The Hon'ble Punjab and Haryana High Court in the case of CIT vs. Haryana Warehousing Corporation 314 ITR 215 held as under:-

“Held. Dismissing the appeal that the deduction claimed by the assessee was legitimate and bonafide in terms of the conflicting determination of law on the proposition in question. The categorical finding at the hands of the Tribunal in its order was that the assessee had disclosed the entire facts without having concealed any income. There was no allegation against the assessee that it had furnished inaccurate particulars of its income. The determination of the Tribunal had not been controverted even in the grounds raised in the appeal. The assessee was guilty of neither of the two conditions. Therefore, in the absence of two pre-requisites postulated under section 271(1)(c) (of Income Tax Act, 1961) it was not open to the revenue to inflict any penalty on the assessee.”

9. The learned CIT(Appeals) considering the material on record correctly followed the decision of the Delhi Bench in the case of AT&T Communications Services (India) Pvt. Limited (supra) for cancelling the penalty against the assessee. The assessee made a bonafide claim of deduction of the expenditure even though it was not acceptable to the revenue, would not lead to inference that assessee has concealed the particulars of income or filed inaccurate particulars of income. Nothing is brought on record if claim of assessee was incorrect in law or was malafide. Therefore, decision relied upon by learned DR is not applicable to the facts of the case.”

5. In CIT vs. Reliance Petroproducts (P) Limited, (2010) 322 ITR 158, the Apex Court was of the view that under section 271(1)(c) (of Income Tax Act, 1961), there has to be concealment of income of the assessee or the assessee must have furnished inaccurate particulars of his income. In the present case, the claim made by the assessee has not been shown to be suffering from any of these conditions. In the absence of any finding recorded by the CIT(A) or the Tribunal with regard to the claim of the assessee that it was malafide, there is no error in cancelling the penalty imposed by the Assessing Officer.

6. Further, reliance of the revenue on the judgment of the Delhi High Court in CIT vs. Zoom Communication (P) Limited, (2010) 327 ITR 510 is of no help to them as therein the High Court was considering the question of levy of penalty under Section 271(1)(c) (of Income Tax Act, 1961) wherein it had concluded to be a case of furnishing of inaccurate particulars of income with malafide intention which is not the case herein.

7. Thus, no substantial question of law arises. The appeal stands dismissed.

(Ajay Kumar Mittal)

Judge

March 16, 2016 (Raj Rahul Garg)

'gs' Judge

×

Similar Ripples

Questions

Tax Penalty Cancelled: Court Upholds Tribunal's Decision in Favor of Assessee

Write your CommentSimilar Posts

Generic

- Reportdata/3002.pdf