Tech Services for Oil Exploration Taxed at 15%, Not 10%

Full News

Tech Services for Oil Exploration Taxed at 15%, Not 10%

Tech Services for Oil Exploration Taxed at 15%, Not 10%

An interesting tax case here. It's about a non-resident company that provided software maintenance services to ONGC (Oil and Natural Gas Commission Limited) for oil exploration. The big question was how much tax they should pay. The court decided they should pay 15% tax instead of 10% because their work counted as "technical services." Let's dive into the details!

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax & Anr. Vs ONGC Ltd (High Court of Uttarakhand)

Income Tax Appeal No. 118 of 2007

Date: 10th April 2008

Key Takeaways:

1. Services for software maintenance in oil exploration count as technical services.

2. Such services are taxed at 15% under Section 44D (of Income Tax Act, 1961) read with Section 115A (of Income Tax Act, 1961), not 10% under Section 44BB (of Income Tax Act, 1961).

3. The distinction between providing services and supplying equipment is crucial for tax purposes.

Issue:

The main question here was: Should the non-resident company's income from providing software maintenance services for oil exploration be taxed at 10% under Section 44BB (of Income Tax Act, 1961) or at 15% under Section 44D (of Income Tax Act, 1961) read with Section 115A (of Income Tax Act, 1961)?

Facts:

1. We've got a non-resident company (NRC) that provided services to ONGC.

2. These services were for maintaining four software modules: ResPrep, ResGram, ResMod, and ResSeis.

3. These software modules were used for exploring, extracting, and producing mineral oils.

4. The case went through several stages: first the Assessing Officer, then the CIT (Appeals), and finally the Income Tax Appellate Tribunal (ITAT).

5. The ITAT's decision was challenged in this High Court appeal.

Arguments:

Here's what each side was saying:

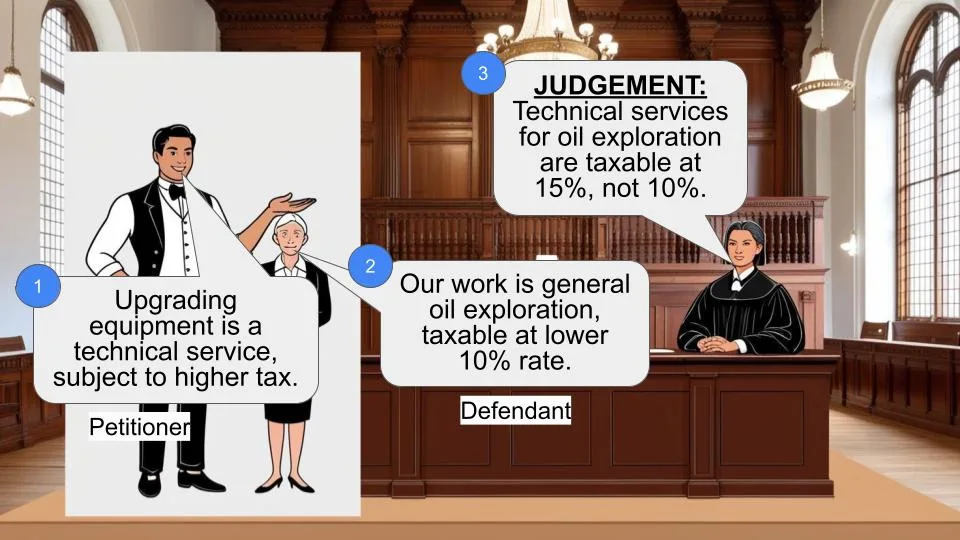

- The non-resident company (assessee) argued: "Hey, we should be taxed at 10% under Section 44BB (of Income Tax Act, 1961) because our work is related to oil exploration."

- The tax department (revenue) said: "Nope, you're providing technical services, so you should be taxed at 15% under Section 115A (of Income Tax Act, 1961) read with Section 44D (of Income Tax Act, 1961)."

Key Legal Precedents:

In this case, the court didn't cite specific precedents. Instead, they focused on interpreting the relevant sections of the Income Tax Act, 1961. The key sections were:

1. Section 44BB (of Income Tax Act, 1961) (10% tax rate for certain oil exploration services)

2. Section 44D (of Income Tax Act, 1961) (special provision for computing income from technical services)

3. Section 115A (of Income Tax Act, 1961) (tax rates for foreign companies)

4. Section 9(1)(vii) (of Income Tax Act, 1961) (definition of "fees for technical services")

Judgement:

The court sided with the tax department. Here's the breakdown:

1. The services provided by the non-resident company were indeed technical services.

2. The company didn't supply any plant or machinery; they just provided software maintenance.

3. Therefore, they should be taxed at 15% under Section 44D (of Income Tax Act, 1961) read with Section 115A (of Income Tax Act, 1961).

4. The court set aside the ITAT's order and upheld the original assessment by the Assessing Officer and CIT (Appeals).

FAQs:

Q1: What's the difference between Section 44BB (of Income Tax Act, 1961) and Section 44D (of Income Tax Act, 1961)?

A1: Section 44BB (of Income Tax Act, 1961) applies to services related to oil exploration and production, taxed at 10%. Section 44D (of Income Tax Act, 1961) is for technical services, taxed at 15%.

Q2: Why didn't the court apply Section 44BB (of Income Tax Act, 1961) in this case?

A2: The court found that the company only provided technical services (software maintenance) without supplying any equipment, so it didn't fall under Section 44BB (of Income Tax Act, 1961).

Q3: What's the significance of this ruling for other companies?

A3: Companies providing software or technical services for oil exploration should be aware that they might be taxed at the higher rate of 15% instead of 10%.

Q4: Does this ruling apply to all services in the oil and gas sector?

A4: Not necessarily. It depends on whether the service is purely technical or involves supplying equipment as well.

Q5: Can the non-resident company appeal this decision?

A5: Potentially, yes. They could try to appeal to a higher court if they believe there's a significant legal issue to be addressed.

This appeal, preferred under Section 260A (of Income Tax Act, 1961), is directed against the judgment and order dated 09.02.2007, passed by Income Tax Appellate Tribunal, Delhi Bench ‘E’ (hereinafter referred as ITAT), whereby the order dated 26.08.2004, passed by Commissioner of Income Tax Appeals (hereinafter referred as CIT (Appeals), Dehradun, is set aside. CIT (Appeals) dismissed the appeal of the assessee and affirmed the assessment order passed by the Assessing Officer under Section 143(3) (of Income Tax Act, 1961).

(2) Heard learned counsel for the parties.

(3) Brief facts of the case are that Oil & Natural Gas Commission Limited (hereinafter referred as ONGC) is representative of the non-resident company (hereinafter referred as NRC)-respondent assessee in the case. The assessee has rendered its services to ONGC for the purposes of exploration, extraction and production of mineral oils. During the year under consideration, the assessee NRC was engaged by ONGC for rendering services in connection with maintenance of ResPrep, ResGram, ResMod, and ResSeis being four modules of software.

(4) The case of assessee is that tax is to be charged on the income of assessee under Section 44BB (of Income Tax Act, 1961), while that of the revenue / present appellant, is that the assessee has rendered the technical services for which he has been paid fee and his case is covered under Section 115A (of Income Tax Act, 1961) read with Section 44D (of Income Tax Act, 1961).

(5) The question of law involved in this appeal is that whether in respect of the receipts for the aforementioned services rendered by NRC, the tax is chargeable under Section 44BB (of Income Tax Act, 1961), or under Section 115A (of Income Tax Act, 1961) read with section 44D (of Income Tax Act, 1961)?

(6) Before Further discussions, we think it just and proper to quote the relevant provision of law referred by the parties. Sub section (1) of Section 44BB (of Income Tax Act, 1961) reads as under:-

”44BB. (1) Notwithstanding anything to the contrary contained in sections 28 to 41 and sections 43 and 43A, in the case of an assessee, being a non resident, engaged in the business of providing services or facilities in connection with, or supplying plant and machinery on hire used, or to be used, in the prospecting for, or extraction or production of, mineral oils, a sum equal to ten per cent of the aggregate of the amounts specified in sub section (2) shall be deemed to be the profits and gains of such business chargeable to tax under the head “ Profits and gains of business or profession”.

Provided that this sub-section shall not apply in a case where the provisions of section 42 (of Income Tax Act, 1961) of section 44D (of Income Tax Act, 1961) or section 115A (of Income Tax Act, 1961) or section 293A (of Income Tax Act, 1961) apply for the purposes of computing profits or gains or any other income referred to in those sections.” The above sub-section (1) of Section 44BB (of Income Tax Act, 1961) contains the proviso quoted above which provides that the sub-section would not apply where the provisions of 42, 44D, 115A or 293A are applicable in computing the profits and gains or income of the assessee. Learned counsel for the appellants has argued that since the assessee has only rendered technical services for which he has been paid the fee as such his case is covered under section 115A (of Income Tax Act, 1961) read with Section 44D (of Income Tax Act, 1961). Section 44D (of Income Tax Act, 1961) contains special provision for computing income by way of royalties or fee for technical services, in the case of foreign companies. Section 115A (of Income Tax Act, 1961) provides the rates of tax on dividends, royalties and technical service fee in the case of foreign companies. In both the sections an explanation has been added clarifying that expression “fees for technical services” shall have same meaning as in the case of explanation 2 to clause (vii) of sub-section (1) of Section 9 (of Income Tax Act, 1961). Said explanation 2 of clause (vii) of sub-section (1) of Section 9 (of Income Tax Act, 1961) reads as under:-

“Explanation 2. For the purposes of this clause “ fees for technical services” means any consideration (including any lump sum consideration) for the rendering of any managerial, technical or consultancy services (including the provision of services of technical or other personnel) but does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head “Salaries”.

(7) Learned counsel for respondent argued that the services rendered by the assessee respondent relate to upgradation of plant and machineries for the purposes of drilling and oil exploration. However, it is not the case of the respondent assessee that the plants and machineries were supplied by it during the Assessment Year, as such the services rendered by NCR assessee is nothing but the technical services rendered by it in the work of oil exploration for which he has charged the fee.

(8) In the above circumstances, we are of the opinion that CIT (Appeals) has not committed any error of law in passing the order dated 26.08.2004 and uphold the view taken by the CIT (Appeals) and that of Assessing Officer whereby the assessee as a technical service provider has been directed to pay tax at the rate of 15 per cent under Section 44D (of Income Tax Act, 1961) read with Section 115A (of Income Tax Act, 1961), instead of 10 percent chargeable under Section 44BB (of Income Tax Act, 1961). The appeal is allowed. Impugned order dated 09.02.2007, passed by ITAT in ITA No. 5098/Del/2004, is set aside. The substantial question of law accordingly stands answered.

(Dharam Veer, J.) (Prafulla C. Pant, J.)

×

Similar Ripples

Questions

Tech Services for Oil Exploration Taxed at 15%, Not 10%

Write your CommentSimilar Posts

Generic

- Reportdata/4661.pdf