Trust Registration Triumph: Court Upholds Tax Exemption Without Local Trust Act…

Full News

Trust Registration Triumph: Court Upholds Tax Exemption Without Local Trust Act Compliance

Trust Registration Triumph: Court Upholds Tax Exemption Without Local Trust Act Compliance

This case involves the Commissioner of Income Tax appealing against M/s Maharashi World Peace Trust. The main dispute was whether the trust needed to be registered under the local Madhya Pradesh Public Trust Act to obtain tax exemption registration under Section 12AA (of Income Tax Act, 1961). The Income Tax Appellate Tribunal (ITAT) ruled in favor of the trust, and the High Court dismissed the appeal, upholding the ITAT's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs M/s Maharashi World Peace Trust (High Court of Madhya Pradesh)

I.T.A No.61/2019

Date: 6th January 2020

Key Takeaways:

1. Registration under local trust laws is not mandatory for obtaining tax exemption under Section 12AA (of Income Tax Act, 1961).

2. The Income Tax authorities should focus on the objects and genuineness of trust activities rather than local law compliance when considering tax exemption applications.

3. The court's decision emphasizes a more inclusive approach to granting tax exemptions to charitable organizations.

Issue:

Is registration under the local Madhya Pradesh Public Trust Act mandatory for a trust to be eligible for registration under Section 12AA (of Income Tax Act, 1961)?

Facts:

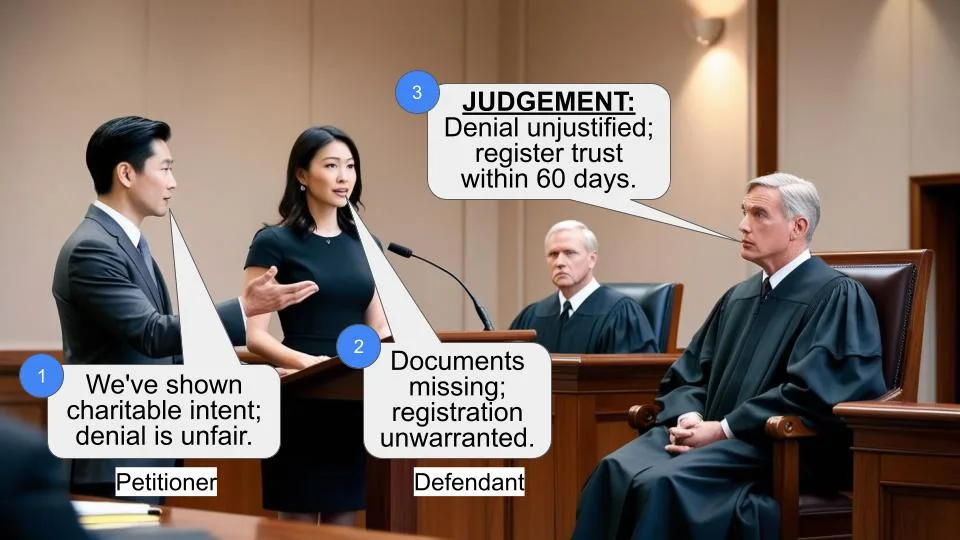

1. M/s Maharashi World Peace Trust applied for registration under Section 12AA(1)(b)(i) (of Income Tax Act, 1961).

2. The Commissioner of Income Tax (Exemptions) [CIT(E)] rejected the application because the trust wasn't registered under the Madhya Pradesh Public Trust Act.

3. The trust appealed to the Income Tax Appellate Tribunal (ITAT), which set aside the CIT(E)'s order and allowed the trust's appeal.

4. The Department of Income Tax then filed this appeal in the High Court against the ITAT's decision.

Arguments:

Department's Arguments:

1. The trust failed to produce a satisfactory reply or certificate of registration under the MP Public Trust Act.

2. Compliance with local laws (MP Public Trust Act) is necessary to prove the genuineness of trust activities.

Trust's Arguments (implied from the judgment):

1. Registration under the local trust act is not a requirement under Section 12AA (of Income Tax Act, 1961).

2. The focus should be on the objects and genuineness of the trust's activities, not local law compliance.

Key Legal Precedents:

The judgment doesn't mention any specific legal precedents. Instead, it focuses on interpreting Section 12AA (of Income Tax Act, 1961).

Judgement:

1. The High Court dismissed the appeal, upholding the ITAT's decision.

2. The court agreed with the ITAT that there is no mandatory requirement for a trust to be registered under local laws before applying for registration under Section 12AA (of Income Tax Act, 1961).

3. The court emphasized that the Income Tax authorities should focus on the objects of the trust and the genuineness of its activities, rather than local law compliance.

4. The court found no infirmity in the ITAT's order and concluded that no substantial question of law arose for consideration.

FAQs:

1. Q: Does this judgment apply to all states in India?

A: While the case specifically dealt with the Madhya Pradesh Public Trust Act, the principle could potentially apply to similar situations in other states.

2. Q: Does this mean trusts don't need to register under local laws at all?

A: No, this judgment only relates to eligibility for tax exemption under the Income Tax Act. Trusts may still need to comply with local laws for other purposes.

3. Q: What should Income Tax authorities focus on when considering applications under Section 12AA (of Income Tax Act, 1961)?

A: They should primarily focus on the objects of the trust and the genuineness of its activities, rather than registration under local laws.

4. Q: Can the Income Tax Department appeal this decision further?

A: Yes, they could potentially appeal to the Supreme Court if they believe a substantial question of law still exists.

5. Q: Does this decision change the requirements for existing registered trusts?

A: No, this decision doesn't affect existing registrations. It clarifies the requirements for new applications and similar cases under review.

1. This appeal has been filed under Section 260-A (of Income Tax Act, 1961) (for short “the Act”) challenging the order dated 12.10.2018 passed by the Income Tax Appellate Tribunal (for short “the Tribunal”), Indore in ITA No.553/Ind/2017 whereby the appeal filed by the assessee was allowed and the order passed by the CIT(E), Bhopal was set aside.

2. The appellant has claimed the following substantial questions of law:-

“1. Whether, on the facts & circumstances of the case, and in law, the ITAT is correct in holding that a public charitable Trust does not require to comply with local law of MP requiring registration under MP Public Trust Act 1951 ?

2. Whether, on the facts and in the circumstances of the case and in law, the ITAT is correct in holding that genuineness of the activities of the trust does not include compliance with requirement of local law namely MP Public Trust Act ?”

3. Briefly stated, the facts of the case are that the respondent-M/s Maharashi World Peace Trust (for short “the assessee Trust”) applied for registration under Section 12AA(1)(b)(i) (of Income Tax Act, 1961) before the CIT(E), Bhopal. The said application was rejected on the ground that the assessee Trust was not registered as a public Charitable Trust. The order passed by the CIT(E), Bhopal was challenged in an appeal before the Tribunal, who in turn, set aside the order passed by the CIT(E), Bhopal and allowed the appeal filed by the assessee Trust holding that the action of learned CIT(E), Bhopal denying the registration merely for the reason that the assessee trust was not registered as Public Charitable Trust cannot be held to be justified. Being aggrieved by the said order of the Tribunal, the department has preferred the present appeal.

4. Learned counsel for the appellant/Department submitted that during the pendency of the application under Section 12AA (of Income Tax Act, 1961), the assessee Trust was required to produce copy of registration as Public Charitable Trust but neither the satisfactory reply nor the certificate of registration as Public Charitable Trust with the Registrar of Madhya Pradesh Public Trust was submitted by it. It was further submitted that the learned Tribunal has erred in holding that genuineness of the activities of the trust does not include compliance with the requirement of local law namely M.P. Public Trust Act.

Further, the Tribunal did not controvert the ground on which the approval was denied by the CIT(E), Bhopal. Accordingly, it was prayed that this appeal may be allowed by setting aside the order impugned in this appeal.

5. Having heard learned counsel for the appellant/Department, we are of the considered opinion that the present appeal deserve to be dismissed.

6. The learned Tribunal while dealing with the argument of learned counsel for the assessee Trust regarding rejection of application filed under Section 12AA (of Income Tax Act, 1961) for the reason that the assessee Trust was not registered as a Public Trust as per M.P. Public Trust Act, 1951 has negatived the said finding of the CIT(E), Bhopal and held as under:-

“6. As per the provisions of Section 12AA(1) (of Income Tax Act, 1961) provides that “Principal Commissioner or Commissioner, on receipt of application for registration of the Trust or Institution made under Clause a or Clause aa of Sub-Section 1 (of Income Tax Act, 1961) of Section 12A (of Income Tax Act, 1961) can call for such documents or information as he thinks necessary in order to satisfy himself about the objects and genuineness of activities of the Trust or Institution and also make such enquiries as he may deem necessary in this behalf and after satisfying himself about the objects of the Trust or Institution and the genuineness of its activities he may pass an order in writing registering the Trust or Institution or if he is not so satisfied, he may pass an order in writing refusing to register the Trust or Institution. Provision of Section 12AA(1) (of Income Tax Act, 1961) refers to the “Trust or Institution”. There seems to be no requirement for a trust to be mandatorily registered as a Public Charitable trust in the State of India where it is located. The action of Ld. CIT-Exemptions denying the registration merely for the reason that the assessee Trust was not registered as a public Charitable Trust cannot be held to be justified.”

7. In the present case, the registration was applied for by the respondent under Section 12AA(1)(b)(i) (of Income Tax Act, 1961) and the provisions under Section 12AA(1) (of Income Tax Act, 1961) also refers to the “trust or institution” and there is no mandate under Section 12AA (of Income Tax Act, 1961) that the application seeking exemption is required to be applied only by a registered Trust or Institution under the local laws i.e. M.P. Public Trust Act, 1951. The learned Tribunal considering the provisions of Section 12AA(1) (of Income Tax Act, 1961) has specifically held that for registering the Trust or Institution for the purposes of the said Act, the Principal Commissioner or Commissioner, is required to satisfy itself about the objects of the applicant – Trust or Institution and the genuineness of its activities. Under the said provision, there is no requirement for a Trust to be mandatorily registered as a Public Charitable Trust under the local Act. In the absence of any provision requiring registration as a Public Charitable Trust before applying for registration under Section 12AA(1) (of Income Tax Act, 1961), the findings arrived at by the learned Tribunal cannot be faulted and said to be illegal or perverse in any manner.

8. In view of the aforesaid, we do not find any reason to take a different view from the one taken by the learned Tribunal as there was no statutory requirement under the Act for the assessee Trust to get itself registered under any law before applying for registration. No infirmity could be found in the order of learned Tribunal warranting interference. Therefore, no substantial question of law arises for consideration.

9. Accordingly, this appeal stands dismissed.

(Ajay Kumar Mittal) (Vijay Kumar Shukla)

Chief Justice Judge

×

Similar Ripples

Questions

Trust Registration Triumph: Court Upholds Tax Exemption Without Local Trust Act Compliance

Write your CommentSimilar Posts

Generic

- Reportdata/6334.pdf