Trust Wins Registration: Court Overturns Tax Commissioner's Denial Based on Doc…

Full News

Trust Wins Registration: Court Overturns Tax Commissioner's Denial Based on Document Filing

Trust Wins Registration: Court Overturns Tax Commissioner's Denial Based on Document Filing

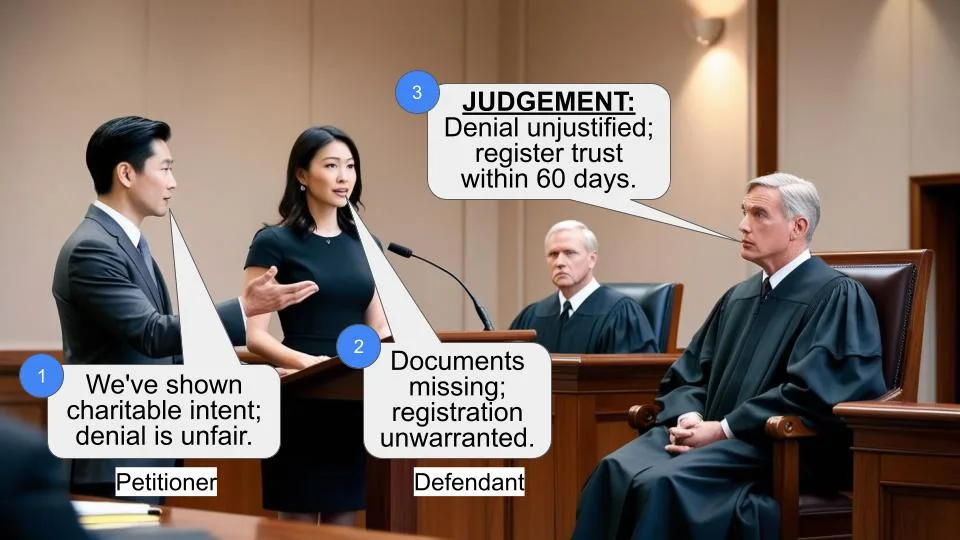

This case involves a dispute between the Commissioner of Income Tax and Shivbachan Singh Samajothan Charitable Trust. The Commissioner denied registration to the trust, citing insufficient documentation. However, the High Court overturned this decision, ruling that the denial was unjustified when no other objections were raised about the trust's activities.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Shivbachan Singh Samajothan Charitable Trust (High Court of Allahabad)

Income Tax Appeal No. 117 of 2016

Date: 16th November 2016

Key Takeaways

1. Non-filing of documents alone is insufficient grounds to deny registration to a charitable trust.

2. The Commissioner must consider the overall genuineness of the trust's activities.

3. If no other objections are raised about the trust's activities, registration should be granted.

4. The court can set a deadline for registration, after which it's deemed granted if not processed.

Issue

Was the Commissioner of Income Tax justified in denying registration to the Shivbachan Singh Samajothan Charitable Trust based solely on the non-filing of certain documents?

Facts

1. Shivbachan Singh Samajothan Charitable Trust applied for registration under section 12AA (of Income Tax Act, 1961).

2. The trust submitted a registered sale deed for the purchase of land to establish a degree college.

3. The Commissioner of Income Tax denied registration, citing insufficient documentation.

4. The trust appealed this decision.

Arguments

Appellant (Commissioner of Income Tax):

- The material placed before the Commissioner was insufficient to determine the status of the trust's activities.

- The trust failed to produce documents substantiating the establishment of a degree college for charitable purposes.

Respondent (Shivbachan Singh Samajothan Charitable Trust):

- The trust had submitted the required evidence, including the sale deed for land purchase.

- No other objections were raised about the genuineness of the trust's activities.

Key Legal Precedents

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to Section 12AA(1)(a) (of Income Tax Act, 1961), which empowers the Commissioner to call for necessary information and make inquiries to satisfy himself about the genuineness of the trust's activities.

Judgment

The High Court ruled in favor of the Shivbachan Singh Samajothan Charitable Trust:

1. The court found that the Commissioner's decision was incorrect.

2. It noted that the trust had submitted the required evidence for land purchase.

3. The court directed the Commissioner to grant registration to the trust under section 12AA(1)(b) (of Income Tax Act, 1961) within 60 days.

4. If registration is not granted within this period, it will be deemed as granted.

FAQs

Q1: Why did the court overturn the Commissioner's decision?

A: The court found that apart from the non-filing of documents, no other objections were raised about the genuineness of the trust's activities. This alone was not sufficient grounds to deny registration.

Q2: What documents did the trust submit?

A: The trust submitted a registered sale deed for the purchase of land intended for establishing a degree college.

Q3: What powers does the Commissioner have under Section 12AA(1)(a) (of Income Tax Act, 1961)?

A: The Commissioner can call for information and make inquiries to satisfy himself about the genuineness of the trust's activities.

Q4: What happens if the Commissioner doesn't grant registration within 60 days?

A: If registration is not granted within 60 days of the court's order, it will be deemed as granted automatically.

Q5: Does this case set any new legal precedent?

A: While it doesn't establish a new precedent, it reinforces the principle that registration shouldn't be denied solely based on documentation issues if there are no other concerns about the trust's activities.

Heard Shri Alok Mathur, learned counsel for the appellant . The contention raised is that the appellate order impugned herein fails to appreciate the fact that the assessee, apart from the sale deed had not been able to produce any document to substantiate the fact of the degree college being established for a charitable purpose.

The appellate authority while proceeding to consider this aspect has held as under.

"It is apparent that the CIT has given an incorrect finding. The assessee has duly submitted the evidence for the purchase of land for the establishment of degree college therefore, in our considered opinion, rejecting the genuineness of the activities merely on the basis that the asseessee failed to submit the documents for the purchase of land for the establishment of degree college under section 12(1)(a) (of Income Tax Act, 1961), no doubt the CIT is empowered to call for such information from the trust or institution as he thinks necessary in order to satisfy himself about the genuineness of the activities of the trust or may also make such inquiry as he may deem necessary in this behalf. In view of this provision, the CIT is empowered to look into whether the assessee trust is charitable or religious in nature. He has also to be satisfied about the genuineness of the activities off the assessee trust. For satisfying himself about thegenuineness of the activities, he is empowered to call for such documents as he may deem fit. We noted that the CIT has not doubted the charitable activities carried on by the assessee.

The only basis on which the registration was not granted to the assessee trust is that the CIT is not satisfied about the genuineness of the activities of the assessee. For giving this finding, the CIT only relied that the assessee has not submitted the documents for the purchase of land for the establishment of degree college but we noted from the documents available on record that the assessee has duly complied with the requirement as desired by CIT. The assesse has duly submitted the copy of registered sale deed for purchase of land for establishment of degree college. Except this there is no objection being made by CIT about the genuineness of the activities of the assessee trust. Thus, in our opinion, the assessee fulfils botht he conditions as has been stipulated under section 12AA(1)(a) (of Income Tax Act, 1961). We, therefore, set aside the order of CIT and direct him to allow registration to the assessee trust under section 12 (of Income Tax Act, 1961) AA (1) (b) of the Act within a period of 60 days from the date of receipt of this order. In case the CIT (Exemption) fails to grant registration to teh assessee trust within the aforesaid period then it will be deemed as the registration has duly been granted to the assessee under section 12AA(1)(b) (of Income Tax Act, 1961). Thus the appeal relating to grant of registration under section 12 (of Income Tax Act, 1961) AA (a) (1) (b) is allowed."

We have considered the submissions raised.

Learned counsel for the appellant submits that as a matter of fact the material that was placed before the Commissioner Income tax was not sufficient enough to record a satisfaction with regard to the status of the activities of the assessee, and in such circumstances the matter ought to have been remanded back to the authority afresh.

We are unable to agree with the submissions inasmuchas the impugned order categorically records that except for the fact of non filing of documents no other objection had been raised by the Commissioner Income Tax about the genuineness of the activities of the assessee trust. In such a situation, such a finding of fact having been recorded and without there being any element of perversity in the same or any other adverse material on record there is no reason to accept the argument of the learned counsel for the appellant as they do not raise any substantial question of law.

The appeal is accordingly rejected.

Order Date :- 16.11.2016

×