Full News

5-Minute Digest: Grasp the Core of 16 CBIC Circulars that Emerged from the Outcomes of 53rd GST Council Meeting

5-Minute Digest: Grasp the Core of 16 CBIC Circulars that Emerged from the Outcomes of 53rd GST Council Meeti…

On June 26, 2024, the Central Board of Indirect Taxes and Customs (CBIC) rolled out a series of circulars following the 53rd GST Council meeting. These circulars, often wrapped in complexity and length, tackle 16 key GST issues. But here's the kicker: you don't have to sift through the legal jargon. Each circular has been boiled down to its essence, enabling you to grasp the core of each one in less than 5 minutes, even during your chill time. Whether it's the new monetary limits for filing GST appeals, interim solutions for post-supply discount compliance, clarifications on five Input Tax Credit (ITC) issues, or insights on two issues each related to the place of supply, time of supply, related party transactions, and GST liability determinations, you'll get the lowdown on each topic in a snap. Talk about a time-saver!

The CBIC sets new monetary thresholds for filing GST appeals at different judicial levels, aiming to reduce unnecessary litigation and provide taxpayers with greater certainty in their assessments. (Please right click here to delve into the essence.)

Circular No. 208/2/2024-GST addresses 8 issues related to the special procedure for manufacturers of specified commodities, providing flexibility in reporting machine details and clarifying electricity consumption ratings. (Please right click here delve into the essence.)

The CBIC has provided guidance on determining the place of supply for goods sold to unregistered persons, particularly in e-commerce transactions. (Please right click here to delve into the essence.)

CBIC clarifies the valuation of imported services from related parties when the recipient is eligible for full input tax credit, aligning treatment of foreign-related parties with domestic ones in specific scenarios. (Please right click here to delve into the essence.)

Circular No. 211/5/2024-GST provides crucial clarification on the time limit for availing Input Tax Credit (ITC) for supplies received from unregistered persons under Reverse Charge Mechanism (RCM). (Please right click here to delve into the essence.)

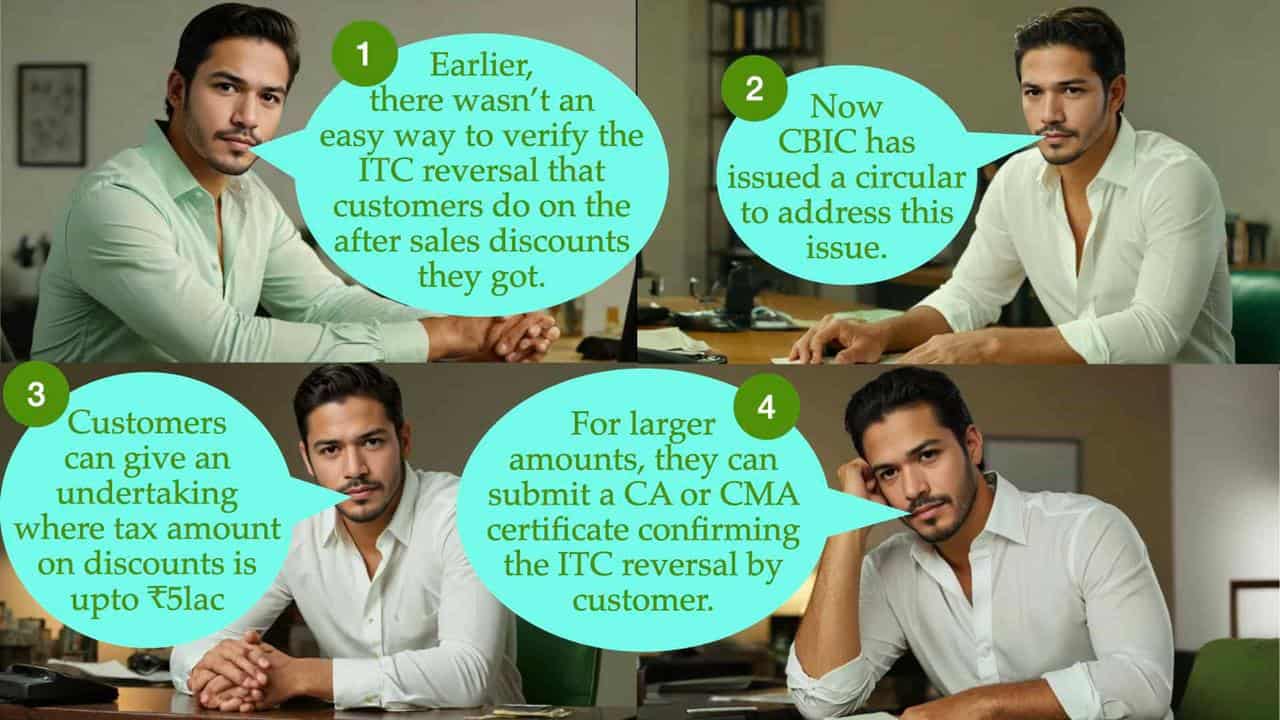

The circular provides a solution for proving Input Tax Credit reversal on post-sale discounts, offering options for certification by CA/CMA or customer undertakings based on discount amounts. (Please right click here to delve into the essence.)

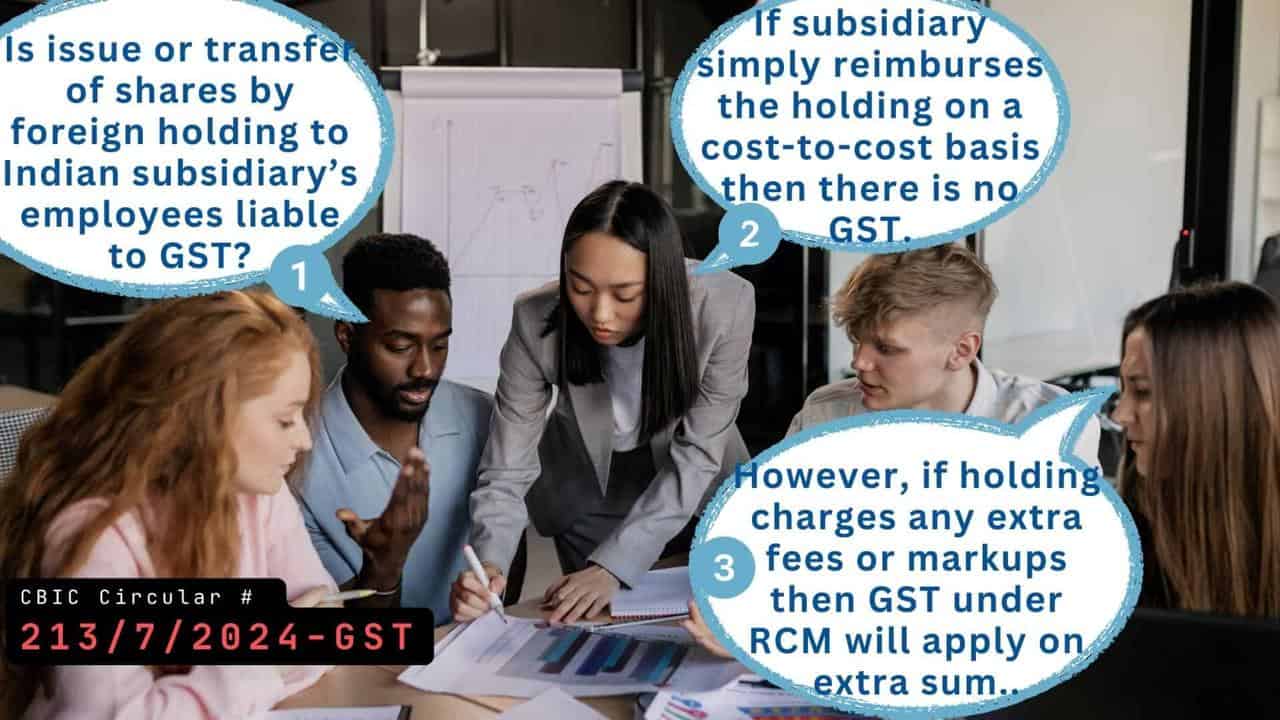

CBIC clarifies that transfer of securities/shares as ESOP/ESPP/RSU is not considered a supply under GST, and cost-to-cost reimbursement for such transfers is not subject to GST. (Please right click here to delve into the essence.)

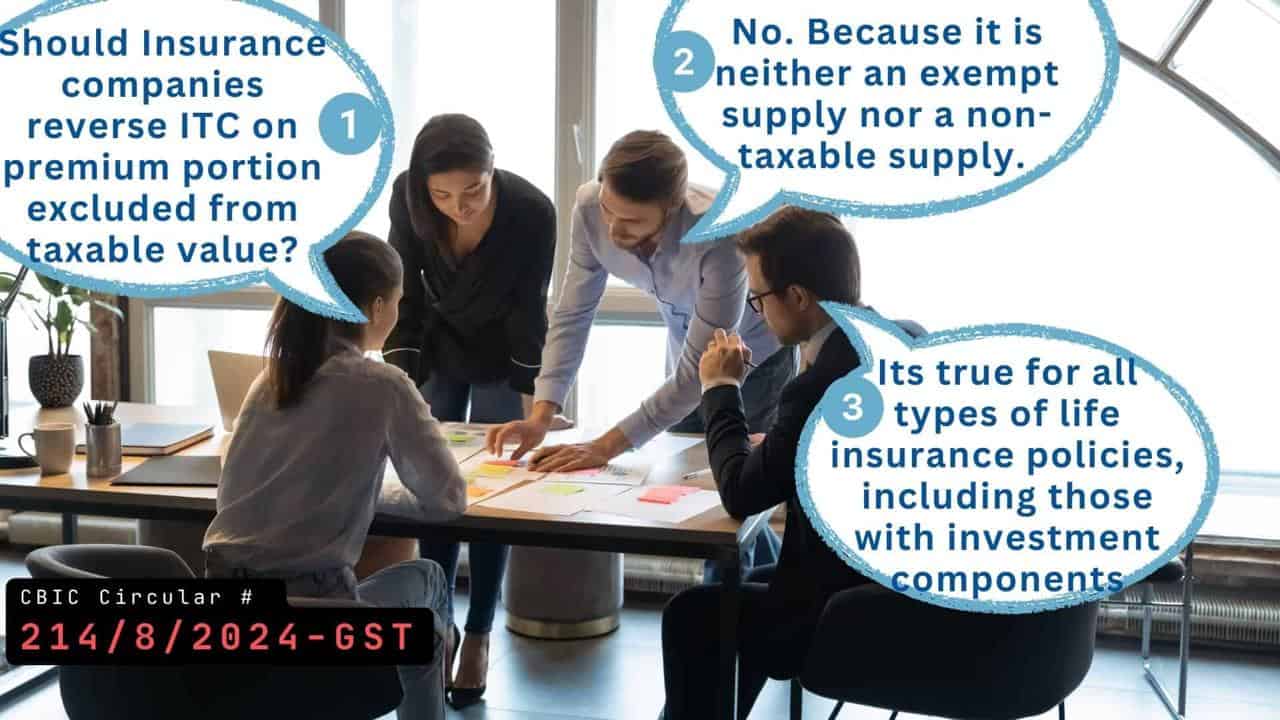

Circular No. 214/8/2024-GST clarifies that the portion of life insurance premiums not included in the taxable value under Rule 32(4) of CGST Rules is neither an exempt nor a non-taxable supply, eliminating the need for input tax credit (ITC) reversal on this amount. (Please right click here to delve into the essence.)

Circular No. 215/9/2024-GST clarifies the GST liability on salvage value in motor vehicle insurance claims, distinguishing between cases where value is deducted from claims and where full claim amount is paid. (Please right click here to delve into the essence.)

Circular No. 216/10/2024-GST provides essential clarifications on GST liability and input tax credit availability for warranty and extended warranty scenarios, addressing various situations including full product replacements, distributor-handled replacements, and the treatment of extended warranties. (Please right click here to delve into the essence.)

The CBIC clarifies that insurance companies can avail Input Tax Credit on repair services for motor vehicles, regardless of whether the claim settlement is through cashless or reimbursement mode, resolving disputes between insurers and tax authorities.(Please right click here to delve into the essence.)

Circular No. 218/12/2024-GST establishes that providing loans to related entities is considered a supply under GST, but the interest or discount on these loans is exempt from GST. (Please right click here to delve into the essence.)

Circular No. 219/13/2024-GST confirms that telecommunication service providers can claim Input Tax Credit on ducts and manholes used in optical fiber cable networks, as these components are considered "plant and machinery" and not restricted under section 17(5) of the CGST Act. (Please right click here to delve into the essence.)

Circular No. 220/14/2024-GST clarifies that custodial services provided by banks to Foreign Portfolio Investors are not considered services to 'account holders'. (Please right click here delve into the essence.)

Circular No. 221/15/2024-GST clarifies that National Highway Projects under the Hybrid Annuity Model (HAM) are considered continuous supply of services, with tax liability arising at invoice issuance or payment receipt, whichever is earlier. (Please right click here to delve into the essence.)

Circular No. 222/16/2024-GST clarifies that spectrum allocation services are considered a continuous supply of services under GST, with tax liability arising at the time of payment due or made, whichever is earlier, for deferred payment options. (Please right click here to delve into the essence.)

×