Court Allows Garden Expenses as Revenue Expenditure for Pollution Control

Full News

Court Allows Garden Expenses as Revenue Expenditure for Pollution Control

Court Allows Garden Expenses as Revenue Expenditure for Pollution Control

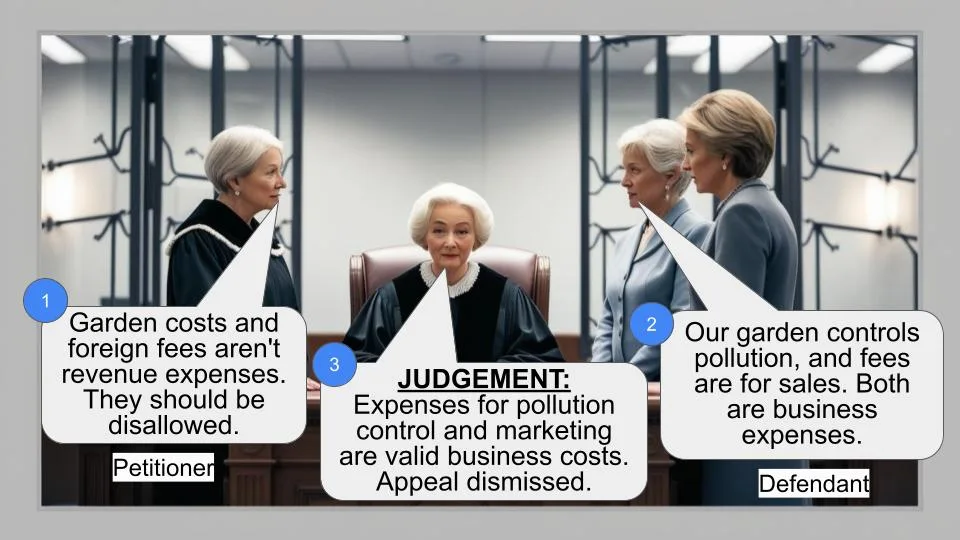

This case involves the Commissioner of Income Tax (appellant) challenging the Income Tax Appellate Tribunal's decision to allow Torrent Pharmaceuticals Ltd. (respondent) to claim garden expenses and foreign registration fees as revenue expenditure. The High Court dismissed the appeal, upholding the Tribunal's decision in favor of the pharmaceutical company.

Case Name:

COMMISSIONER OF INCOME TAX VS TORRENT PHARMACEUTICALS LTD.

( High Court of Gujrat)

Date:30 August 2012

Key Takeaways:

1. Garden expenses incurred for pollution control can be claimed as revenue expenditure.

2. Foreign registration fees for product marketing overseas are allowable as revenue expenses.

3. Expenses with a clear nexus to business activities can be treated as revenue expenditure.

Issue:

Was the Income Tax Appellate Tribunal correct in allowing garden expenses and foreign registration fees to be treated as revenue expenditure for Torrent Pharmaceuticals Ltd.?

Facts:

1. The case pertains to the Assessment Year 1999-2000.

2. The Assessing Officer initially disallowed Rs. 24,32,322/- for garden expenses and Rs. 28,14,355/- for foreign registration fees.

3. The Commissioner of Income Tax (Appeals) allowed both expenses as revenue expenditure.

4. The Income Tax Appellate Tribunal upheld the CIT(A)'s decision.

5. The Revenue department appealed to the High Court under section 260A (of Income Tax Act, 1961).

Arguments:

Appellant (Revenue Department):

- Garden expenses and foreign registration fees should not be treated as revenue expenditure.

Respondent (Torrent Pharmaceuticals Ltd.):

- Garden expenses were necessary for pollution control within the factory premises.

- Foreign registration fees were recurring expenses essential for overseas product marketing.

Key Legal Precedents:

The Tribunal relied on its own decision in the assessee's case (ITA No. 1347 of 2007) for the Assessment Year 2003-2004, where similar garden expenses were allowed as revenue expenditure.

Judgement:

1. The High Court dismissed the appeal, upholding the Tribunal's decision.

2. Garden expenses were justified as they helped control pollution from the effluent treatment plant.

3. Foreign registration fees were considered business expenses as they facilitated overseas product marketing.

4. The court found no substantial question of law arising from the case.

FAQs:

1. Q: Why were garden expenses considered revenue expenditure?

A: The garden helped control pollution from the effluent treatment plant, making it directly related to the business activity.

2. Q: What was the basis for allowing foreign registration fees as revenue expenditure?

A: These fees were recurring expenses necessary for marketing products overseas and promoting sales, thus directly linked to business operations.

3. Q: How did the company's exports change over the years?

A: Exports increased from Rs. 26 crores in 1998-1999 to Rs. 160 crores in 2005-2006, showing a growth of more than 600%.

4. Q: What was the key factor in determining whether an expense could be claimed as revenue expenditure?

A: The court emphasized that expenses with a clear nexus to business activities can be treated as revenue expenditure.

5. Q: Did this case set any new legal precedents?

A: While it didn't set new precedents, it reinforced the principle that expenses directly related to business operations, even if unconventional like gardening for pollution control, can be claimed as revenue expenditure.

The Revenue has preferred the present appeal under section 260A (of Income Tax Act, 1961) against the order dated 11.2.2011 of the Income Tax Appellate Tribunal Ahmedabad Bench 'C' in ITA No. 241 of 2008.

1.1 Following two questions are proposed by the appellant as substantial question of law : “[A] Whether the Appellate Tribunal is right in law and on facts in deleting the disallowance out of garden expenses of Rs.24,32,322/- by treating such expenditure as revenue expenditure?

[B] Whether the Appellate Tribunal is right in law and on facts in directing the Assessing Officer to treat the expenditure of Rs. 28,14,355/- incurred on foreign regisgtration fees as revenue expenses?”

2. We heard learned advocate Ms. Paurami B. Sheth, learned counsel for the appellant.

2.1 At the time of considering the return of income of the respondent-assessee in respect of Assessment Year 1999-2000, the Assessing Officer by his assessment order dated 29.12.2006 disallowed Rs. 24,32,322/- which was the amount debited by the assessee as garden expenses treating it to be a revenue expenditure. Secondly, the assessing officer disallowed Rs. 28,14,355/- as revenue expenditure being the amount with regard to the foreign registration fees. Against the said assessment order, the assessee preferred appeal before the Commissioner of Income Tax (Appeals) which came to be allowed on both the aforesaid counts.

3. For claiming garden expenses as revenue expenditure the explanation of the assessee was that the said expenditure was required to be incurred for gardening inside the factory premise so as to control the pollution. The CIT(A) observed that in the assesse's own case for the Assessment Year 2003-2004, he was given the benefit for such expenditure as revenue expenditure. In respect of the second disallowance, the CIT(A) was of the view that the registration feess in foreign countries for the purpose of export was paid on recurring basis depending upon validity of various registrations and the same would have to be repaid on expiry of registration. According to the CIT(A), the assesse was entitled to treat the said expenditure as revenue expenditure.

3.1 The department preferred an appeal against order of the CIT(A) which culminated into the impugned order. As far as the question of treating garden expenses is concerned, the Tribunal held that the issue was covered in favour of the assessee by its decision in assessee's own case in ITA No. 1347 of 2007 for the Assessment Year 2003-2004. The Tribunal relied on its own observations in para 29 of the judgment in the said appeal and accordingly confirmed the order of the CIT(A). With regard to foreign registration fees, the Tribunal concluded that said expenses were incurred for obtaining registration in the foreign country for marketing the products overseas, which was expenditure for sales promotions, without which the assessee company would not have been able to market its product in the overseas market.

4. The Tribunal in the impugned order recorded the findings inter- alia as under :

“Further, these payments are made to drug regulatory authorities in various countries for the products market in the respective countries. Furthermore, these fees are to be paid on recurring basis depending upon the validity of the various registrations. The fees have been paid on expiry of the registration and out of total payment of Rs. 8,03,706/- is in respect of product registration in Poland. Likewise payments have been made in Vietnam, Russia, Ghana and China etc. We find that the exports over the years have increased from the export sale of Rs. 26 crores in financial year 1998-1999 to the exports have grown to Rs. 160 crores in financial year 2005-2006 an increase of more than 600%. Accordingly, these expenses are rightly allowed by CIT(A) and we confirm the same.”

5. The findings of the Tribunal are justified on both the issues. The garden expenditure was for the purpose of maintaining garden to control the pollution. The company had put up an affluent treatment plant and pollution used to generate because of release of pollutants. The maintaining a garden helped in controlling pollution arising from the pollutants. It cannot be gainsaid that the expenses for garden had nexus with business activity. It can well be treated for business purpose and can be claimed as revenue expenditure. Similarly the expenses for foreign country registration was for business purpose only, because the same helped the assessee in marketing its products in the foreign countries and promoting the sales.

6. For the aforesaid reasons, the Tribunal committed no error. Its findings are proper and in no way are perverse. No substantial question of law arises for consideration.

7. This Tax Appeal is accordingly dismissed.

[V.M.SAHAI, J.]

[N.V.ANJARIA, J.]

×

Similar Ripples

Questions

Court Allows Garden Expenses as Revenue Expenditure for Pollution Control

Write your CommentSimilar Posts

Generic

- Reportdata/5504.pdf