Court Dismisses Penalty for Inaccurate Income Particulars, Citing Lack of Asses…

Full News

Court Dismisses Penalty for Inaccurate Income Particulars, Citing Lack of Assessing Officer's Satisfaction

Court Dismisses Penalty for Inaccurate Income Particulars, Citing Lack of Assessing Officer's Satisfaction

This case involves the Commissioner of Income Tax (Revenue) appealing against an order by the Income Tax Appellate Tribunal. The Tribunal had dismissed the Revenue's appeal regarding a penalty of Rs.10,09,948/- under Section 271(1)(c) (of Income Tax Act, 1961), imposed on the assessee (Societex). The High Court ultimately dismissed the Revenue's appeal, agreeing with the Tribunal's decision that no penalty should be levied.

Case Name**: COMMISSIONER OF INCOME TAX VS SOCIETEX

**Key Takeaways**:

1. Penalties under Section 271(1)(c) (of Income Tax Act, 1961) cannot be levied without the Assessing Officer's recorded satisfaction of inaccurate income particulars.

2. Inadvertent or mechanical errors in tax claims may not warrant penalties.

3. First-time errors or claims without a history of inaccuracies may be viewed more leniently.

**Issue**:

Can a penalty under Section 271(1)(c) (of Income Tax Act, 1961) be levied when the Assessing Officer did not record satisfaction that the assessee was guilty of filing inaccurate particulars of income?

**Facts**:

1. The assessee, Societex, is engaged in consultancy services.

2. For the assessment year 1997-98, they claimed depreciation on properties in Bangalore and Khan Market, New Delhi.

3. The CIT (Appeals) allowed 2/3rd of the depreciation claim for the Bangalore property but disallowed it for the Khan Market property.

4. The assessee had made a provision for taxation of Rs.23,50,000/- under "current liabilities" which was not added back to the profit in the income tax return.

5. The Assessing Officer initiated penalty proceedings under Section 271(1)(c) (of Income Tax Act, 1961)

**Arguments**:

Revenue's Arguments:

- The assessee's behavior showed conscious knowledge of an inadmissible claim.

- The provision for tax is not deductible under any law, warranting a penalty.

Assessee's Arguments:

- The CIT(Appeals) partially accepted the depreciation claim for the Bangalore property.

- The Khan Market property was only let out from August 1996, leading to a mechanical repetition of the claim.

- The provision for taxation claim was inadvertent and made for the first time that year.

**Key Legal Precedents**:

1. CIT vs. Zoom Communication Pvt. Ltd. (2010) 327 ITR 510

2. CIT vs. Escorts Finance Ltd. (2010) 328 ITR 44

3. CIT v. Reliance Petro Products Pvt. Ltd., (2010) 322 ITR 158

These cases suggest that even inadvertent inaccuracies could warrant penalties if the explanation is not bona fide. However, the court distinguished the current case from these precedents.

**Judgement**:

The High Court dismissed the Revenue's appeal, agreeing with the Tribunal's decision. The court reasoned that:

1. The CIT(Appeals) had partially accepted the depreciation claim for the Bangalore property.

2. The Khan Market property was newly let out, explaining the mechanical claim.

3. The provision for taxation claim was made for the first time, indicating no history of inaccuracies.

4. Both the CIT(Appeals) and the Tribunal had ruled in favor of the assessee.

The court concluded that no substantial question of law arose in this case.

**FAQs**:

1. Q: What is Section 271(1)(c) (of Income Tax Act, 1961)?

A: It's a provision that allows for penalties to be imposed for concealing particulars of income or furnishing inaccurate particulars of income.

2. Q: Why did the court dismiss the penalty in this case?

A: The court found that the errors were likely inadvertent or mechanical, and there was no history of furnishing inaccurate particulars in previous years.

3. Q: What's the significance of the Assessing Officer's satisfaction?

A: The court emphasized that penalties under Section 271(1)(c) (of Income Tax Act, 1961) cannot be levied without the Assessing Officer recording their satisfaction that the assessee was guilty of filing inaccurate particulars.

4. Q: How does this judgment impact similar cases?

A: It suggests that courts may be more lenient in cases where errors appear to be inadvertent or first-time occurrences, rather than deliberate attempts to evade taxes.

5. Q: What should taxpayers learn from this case?

A: While inadvertent errors may be viewed leniently, it's crucial to ensure accuracy in tax filings and to provide bona fide explanations for any discrepancies.

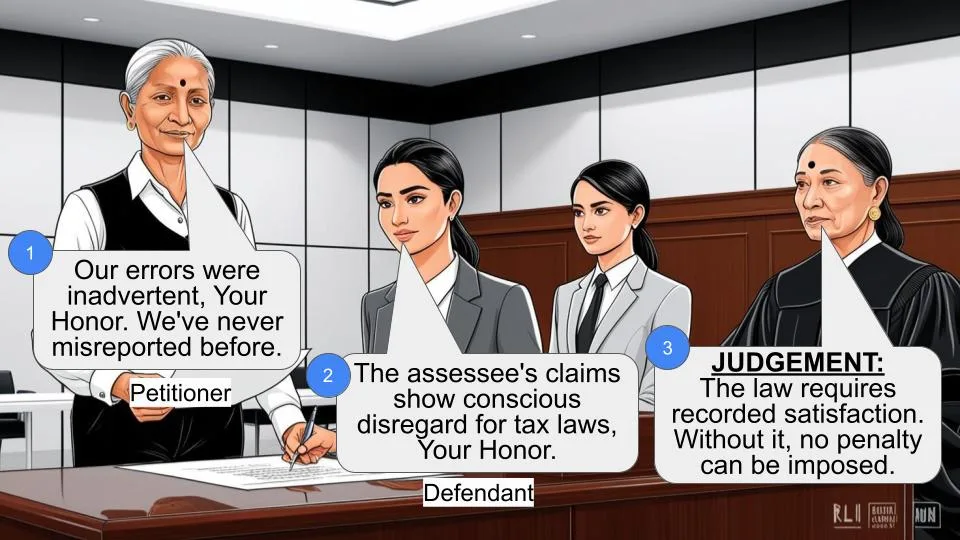

The Revenue claims to be aggrieved by the order dated 25.3.2011 of the Income Tax Appellate Tribunal („Tribunal‟, for short) whereby its appeal was dismissed. It urges that the Tribunal fell into error in holding that the penalty to the extent of Rs.10,09,948/- under Section 271(1)(c) (of Income Tax Act, 1961) („Act‟, for short), was not leviable on the assessee.

2. The assessee is engaged inter alia in rendering consultancy services. It had, for the assessment year 1997-98, claimed depreciation in respect of the properties – one at Bangalore and the other at Khan Market, New Delhi. In the first round, the matter came for the determination of the CIT (Appeals), who concluded that depreciation was allowable only to the extent of 2/3rd claim in respect of the Bangalore property and that for the Khan Market property such deduction could not be claimed.

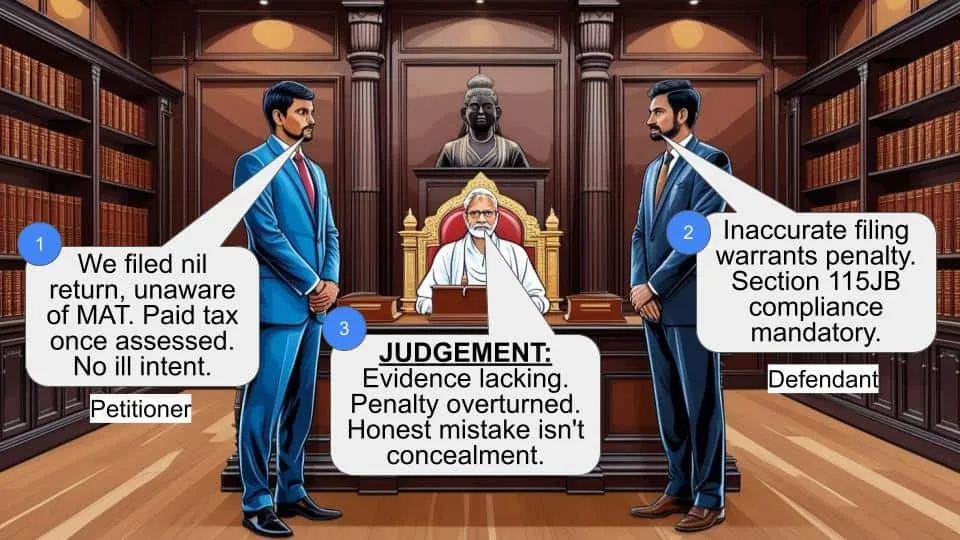

The total amount added back for these were Rs.9,561/- and 1,71,683/-. The assessee had also made provision for taxation to the extent of Rs.23,50,000/- under the head “current liabilities” and the provision was not added back to the profit as per the profit and loss account, in the return of income. In the assessment, this too was disallowed.

In the above circumstances, the Assessing Officer by separate orders initiated penalty proceedings under Section 271(1)(c) (of Income Tax Act, 1961) which culminated in an order of 31.1.2001. The matter was carried in appeal to the CIT (Appeals) who deleted the penalty on the ground that inaccurate particulars in terms of Section 271(1)(c) (of Income Tax Act, 1961) had not been furnished. The Tribunal, on appeal by the Revenue, held that no satisfaction was recorded by the Assessing Officer in the assessment proceedings that the assessee was guilty of filing inaccurate particulars of income and agreed with the CIT (Appeals) on his ground. The Tribunal also examined the levy on merits and held that no penalty was imposable in respect of the depreciation claim vis-à-vis Khan Market and Bangalore properties, but held that penalty was imposable with reference to the claim for deduction of the provision for taxation.

3. The assessee and the revenue filed cross-appeals before this Court in ITA Nos.1332 and 1494/2006. They were disposed of by order of this Court on 29.9.2008 remitting the matter for reconsideration, to the Tribunal, on merits.

4. The Tribunal by its impugned order held that having regard to the circumstances, the penalty could not be levied. The essential reasoning of the Tribunal is to be found in para 6 of its impugned order which reads as follows :

“6. We have heard both the sides. The provision made for advance tax of Rs.23,50,000/- debited in the P&L account not added back to income is bonafide mistake. Assessee paid advance tax in the month of March only. It is the first time that provision was debited in P&L account. Had there been any intention to file inaccurate particulars then the assessee could not have paid the advance tax in the last month of assessment year. The assessee concern is a firm which is not having expert chartered accountants at its payroll. Further, this was the first year in which the provision for taxation was debited to the P&L account. In such a situation, it is a human bonafide clerical mistake occurred while making the statement of income. The assessee rectified the mistake as soon as it was detected. Even the Assessing Officer failed to detect the mistake while making the order u/s 143(1)(a) (of Income Tax Act, 1961). After considering all the relevant facts and circumstances holistically, we hold that the mistake was bonafide and assessee cannot be visited with the penalty u/s 271(1)(c) (of Income Tax Act, 1961) for filing inaccurate particulars of income and the case laws relied upon are also not applicable. Accordingly, the ground is dismissed.”

5. Mr. Maratha relied upon the decision of CIT vs. Zoom Communication Pvt. Ltd. (2010) 327 ITR 510 as well as decision of CIT Vs. Escorts Finance Ltd. (2010) 328 ITR 44. It was urged that in this case, the assessee‟s behaviour was not one of furnishing a claim that was incorrect in law but showed a conscious knowledge of the claim which could not be granted. It was emphasized that under no circumstances the assessee could have claimed provision for tax as that is not deductable under any provision of law. Therefore, the penalty order made by the Assessing Officer was warranted in the circumstances. Ld. counsel also relied upon the decision reported as CIT vs. Escorts Finance Ltd. (supra). Ld. counsel for the assessee contended that it is evident that the CIT(Appeals) has partially accepted the assessee‟s claims to the extent that the depreciation was granted in respect of the Bangalore property. Ld. counsel stressed upon the fact that the Khan Market property had been let out only from August, 1996 and under the circumstances there seems to have been a mechanical repetition of the claim in the return filed. So far as the question of furnishing inaccurate particulars with regard to the provision of taxation is concerned, ld. counsel submitted that it was inadvertent and even the record showed that such a claim had been made for the first time during the assessment year.

6. Zoom Communication Pvt. Ltd. (supra) is premised on the footing that even if inadvertent by particulars are not given, if the authority finds that the explanation given is not bona fide penalty u/s. 271 (of Income Tax Act, 1961) would be warranted. Similar observations were made in CIT v. Reliance Petro Products Pvt. Ltd., (2010) 322 ITR 158. In the present case, so far as the question of depreciation is concerned what emerges from the previous discussion is that the CIT(Appeals) had accepted the assessee‟s claim for depreciation to the extent of 2/3rd in respect of the Bangalore property. It is also the matter of record that the Khan Market property was let out for the first time in the latter part of the concerned assessment year i.e. in August, 1996. In these circumstances, the benefit of inadvertence or mechanical or repetitive claim being made can be given to the assessee. Similarly, as far as the provision for taxation is concerned, we notice that the Tribunal by the impugned order had stated in the extract reproduced above that the assessee had made a claim for deduction of the provision for the first time in the year under appeal; in other words, there was no history of furnishing such accurate particulars by the assessee for the previous years. Having regard to these circumstances and the fact that the CIT(Appeals) as well as the Tribunal had held in favour of the assessee, this Court is of the opinion that no substantial question of law arises in this case. Appeal is dismissed.

S. RAVINDRA BHAT, J.

R.V.EASWAR, J.

×

Questions

Court Dismisses Penalty for Inaccurate Income Particulars, Citing Lack of Assessing Officer's Satisfaction

Write your CommentSimilar Posts

Generic

- Reportdata/5653.pdf