Check your phone. I have messaged an OTP. It is a 6 digit number. Feed it in the box below

Do you want me to resend the OTP? Yes resend it-

Court Allows 100% Tax Deduction for Expanded Units in Himachal Pradesh

The High Court ruled that industrial units in Himachal Pradesh established after January 7, 2003 are eligible for 100% tax deduction under Section 80-IC (of Income Tax Act, 1961) for 5 years after undertaking substantial expansion, subject to an ove…

Login to write your news

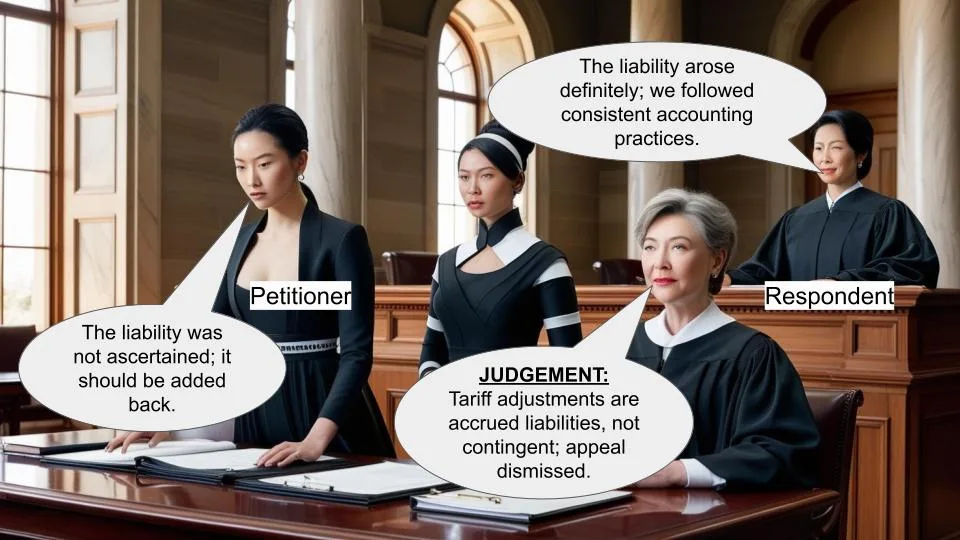

High Court upholds ITAT decision on tariff adjustments in power company's tax c…

This case involves an appeal by the Principal Commissioner of Income Tax against NHPC Ltd., a power company. The dispute centered around the tax treatment of tariff adjustments made by NHPC. The High Court dismissed the appeal, ruling in favor of NH…

Login to write your news

Application of a wrong provision or the erroneous application of the same to th…

Held Effect of Section 199 (of Income Tax Act, 1961) was not considered. Partially, the assessee is to be blamed because such issue was not raised substantially by the assessee. Nevertheless, it being a question of law, the assessee should be per…

Login to write your news

Court strikes down amendment limiting stay orders in tax appeals, reinforcing t…

In the case of Pepsi Foods Pvt. Ltd. Vs Assistant Commissioner of Income Tax & Anr, the court addressed the constitutional validity of a provision in the Income Tax Act that restricted the extension of stay orders beyond 365 days, even if the delay …

Login to write your news

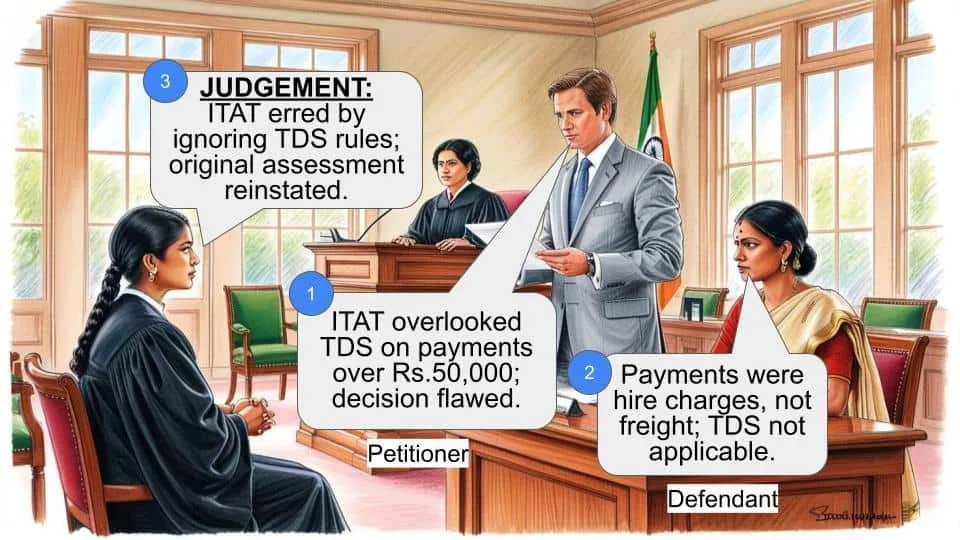

ITAT's Misstep: Tribunal's Decision Overturned on TDS Non-Compliance

In the case of the Commissioner of Income Tax vs. Maruti Subray Patil, the court addressed whether the Income Tax Appellate Tribunal (ITAT) erred in its decision regarding the non-deduction of tax at source (TDS) on payments exceeding Rs.50,000. The…

Login to write your news

Tushar Hemani, Parimalsinh B. Parmar, Vijay Govani, AR and Khyati Chugh, AR for…

Tushar Hemani, Parimalsinh B. Parmar, Vijay Govani, AR and Khyati Chugh, AR for the Assessee. S.S. Shukla for the Revenue.

Login to write your news

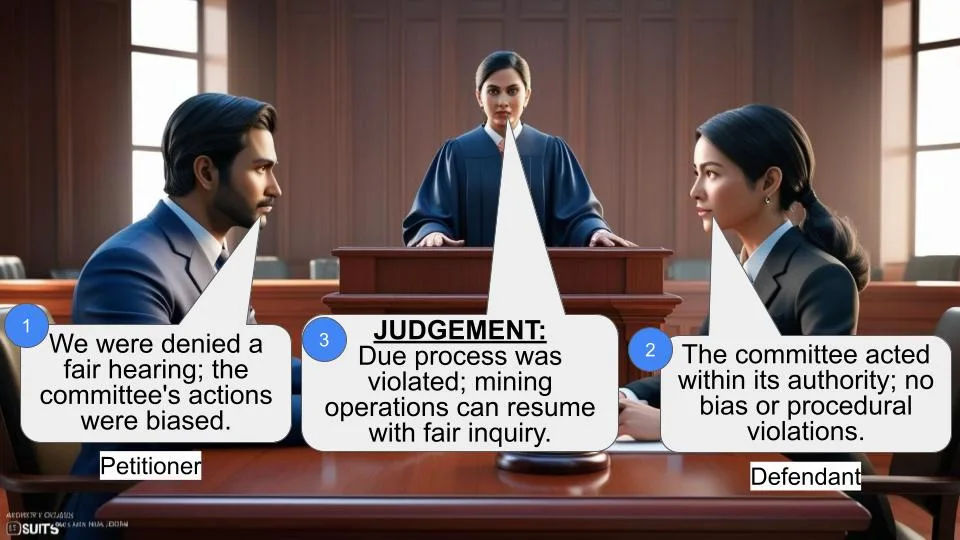

Court rules on mining disputes, emphasizing due process and bias concerns in Ta…

This case involves two writ petitions filed by mining companies, Transworld Garnet India Pvt. Ltd. and V.V. Mineral, against the State of Tamil Nadu regarding allegations of illegal mining. The court addressed issues of procedural fairness, bias in …

Login to write your news

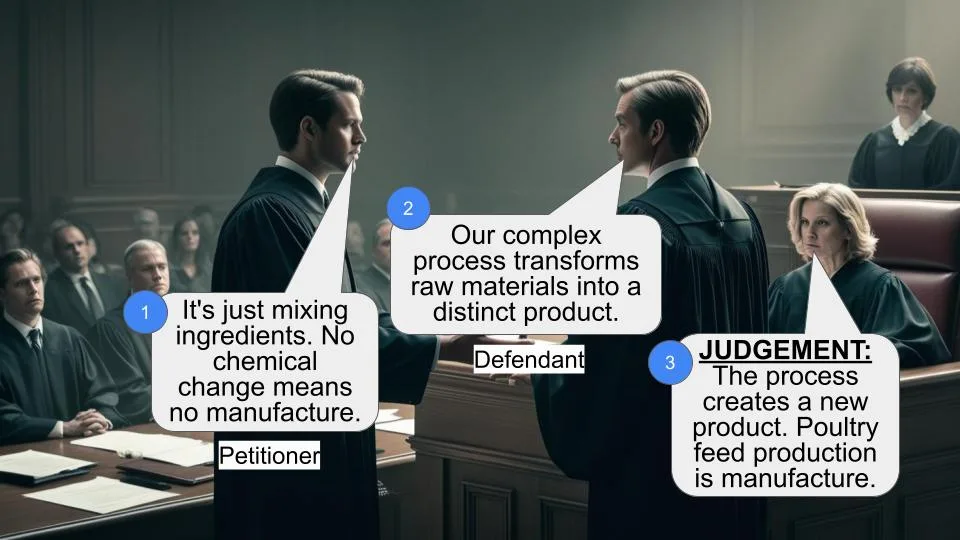

Court Rules Poultry Feed Production Qualifies as 'Manufacture' for Tax Deduction

The case involves a dispute between the Principal Commissioner of Income Tax (Revenue) and Sona Private Ltd. (Assessee) regarding whether the production of poultry feed constitutes 'manufacture' for the purpose of claiming tax deductions under Secti…

Login to write your news

Court Upholds Tax Authority’s Revision of Flawed Assessment Order

This case involves a dispute between a taxpayer and the tax authority over the revision of an assessment order under Section 263 (of Income Tax Act, 1961). The tax authority found the original assessment order to be erroneous and prejudicial to the …

Login to write your news

Prakash Jothwani, A.R for the Appellant. H.N. Singh, D.R for the Respondent

Prakash Jothwani, A.R for the Appellant. H.N. Singh, D.R for the Respondent

Login to write your news

COMMISSIONER OF INCOME TAX (CENTRAL)-I VS VATIKA TOWNSHIP PRIVATE LIMITED-(Supr…

If the enactment is expressed in language which is fairly capable of either interpretation, it ought to be constued as prospective only.

Login to write your news

Court dismisses petition due to lack of evidence on legal advice for appeal wit…

In the case of Jayant D. Sanghavi vs. Income Tax Appellate Tribunal, the High Court dismissed the petitioner's application to recall a previous order dismissing his appeal. The petitioner claimed he withdrew his appeal based on his advocate's advice…

Login to write your news-

Section - 245MA (of Income Tax Act, 1961), Dispute Resolution Committee

Income Tax,Feb. 08, 2023Dispute Resolution Committee.

-

Delhi High Court Upholds Tribunal’s Decision on Carry Forward of Losses

Income Tax,Dec. 14, 2023The High Court of Delhi, in the case of ITA 660/2023, upheld the decision of the Income Tax Appellate Tribunal regarding the carry forward of losses. The court concluded that the Assessing Officer (AO) dealing with the assessment in the subsequent year would decide whether the loss incurred in any year could be carried forward and set off against the profits. The court also noted that unabsorbed depreciation and capital losses are not covered by th…

-

Neera Malhotra for the Appellant. K.Y.Ningoji Rao, CA for the Respondent.

Income Tax,Oct. 28, 2021Neera Malhotra for the Appellant. K.Y.Ningoji Rao, CA for the Respondent.

-

J. P. Khaitan, Sr. Adv. Anupa Banerjee, Adv. Sagnik Basu, Adv. Nidhi Bahal, Adv…

Income Tax,Jun. 27, 2022J. P. Khaitan, Sr. Adv. Anupa Banerjee, Adv. Sagnik Basu, Adv. Nidhi Bahal, Adv. Shivam Pathak, Adv. for the Petitioner. P. K. Bhowmik, Adv. A. Bhowmick, Adv. for the Respondent.

-

Air India vs. Deputy Commissioner: Tribunal's Misstep Leads to Reassessment

Income Tax,Aug. 22, 2020This case involves Air India Ltd. and the Deputy Commissioner of Income Tax (International Taxation). The dispute centers on whether Air India should be treated as a representative assessee for Caribjet Inc., a foreign company, under Section 163 (of Income Tax Act, 1961). The High Court found that the Tribunal's decision to treat Air India as a representative assessee was flawed and ordered a fresh hearing.

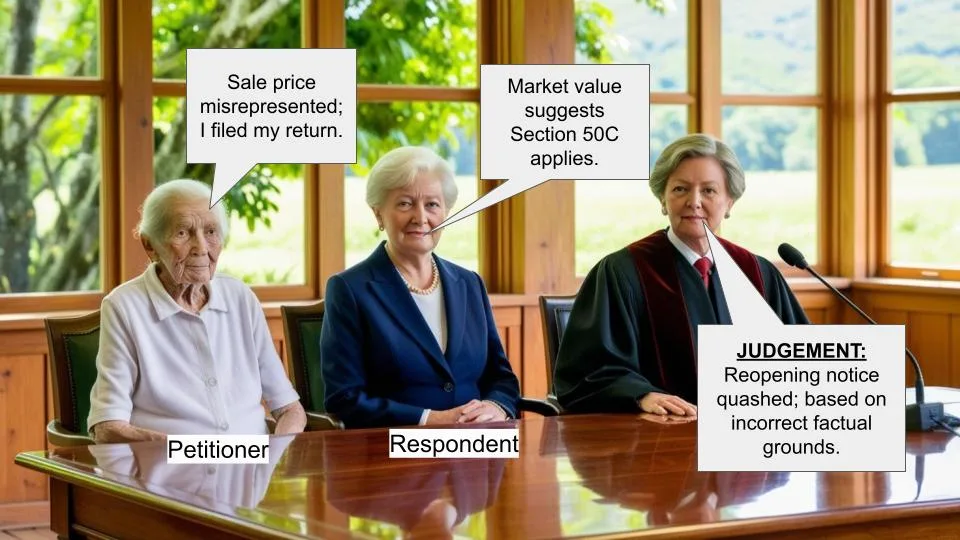

Court quashes reopening notice based on erroneous factual grounds

This case involves a dispute between Mumtaz Haji Mohmad Memon (the petitioner) and the Income Tax Officer (the respondent). The Income Tax Officer issued a notice to reopen the petitioner's assessment for the 2010-11 assessment year, citing reasons that were later found to be factually incorrect. The High Court ultimately quashed the reopening notice, ruling in favor of the petitioner.

Income Tax,Jul. 24, 2020-

Reopening of assessment on the basis of mistaken facts is bad in law.

Income Tax,Jul. 24, 2021Held Before the AO assumes jurisdiction to re-open it is necessary that the conditions laid down in the said section 147 (of Income Tax Act, 1961) has to be satisfied viz., AO should record "reason to believe" that the income chargeable to tax for that assessment year has escaped assessment. (para 7) Even if there is foundation based on information there must be some reason warrant holding the belief that income chargeable to tax has esca…

-

Merely because a fee or some other consideration is collected or received by as…

Income Tax,May. 26, 2021Held It is undisputed fact that the assessee has been granted a valid registration u/s 12AA (of Income Tax Act, 1961) which has never been revoked by the revenue authorities. The registration has been granted post-insertion of proviso to Sec.2(15) (of Income Tax Act, 1961) obviously after looking into the object of the assessee. (para 8.1) At the time of passage of the PSS Bill, 2006 the then Hon'ble Finance Minister, inter-alia, reiterate…

A.O. would not get assumption of jurisdiction legally to frame the re-assessmen…

Income Tax,Jun. 28, 2021It is well settled Law that validity of the reopening of the assessment is to be determined with reference to the reasons recorded for reopening of the assessment. The assessee has filed copy of the reasons recorded for reopening of the assessment in the paper book which is reproduced above in which the A.O. has mentioned that he has information that assessee has deposited cash amounting to RS.11,07,160/- with ICICI Bank Ltd., and also received co…

Sudhir Sehgal, Adv. for the Assessee. C. Chandrakanta, CIT (DR) for the Revenue.

Sudhir Sehgal, Adv. for the Assessee. C. Chandrakanta, CIT (DR) for the Revenue.

Income Tax,Apr. 20, 2021-

Income Tax , May. 08. 2021

U.S. Yogesh Kumar, Advocate for the Appellant. Ganesh B.Ghale, Standing Counsel…

-

Income Tax , Sep. 19. 2020

Income Tax , Sep. 19. 2020Court Clarifies ‘Salary’ Definition for Gratuity and Leave Encashment Exemptions

-

Income Tax , Mar. 06. 2021

Income Tax , Mar. 06. 2021Delay Condoned: Court Prioritizes Justice Over Procedural Lapses

-

Income Tax , Jun. 01. 2021

Income Tax , Jun. 01. 2021Vijay Jindal, CA for the Petitioner. Rakhi Vimal, SR. DR for the Respondent.

-

Income Tax , Oct. 17. 2020

Income Tax , Oct. 17. 2020LIBERTY INDIA VS COMMISSIONER OF INCOME TAX_(Supreme Court)