Court Upholds Time Limit for Tax Settlement Rectification, Dismisses Late Appli…

Full News

Court Upholds Time Limit for Tax Settlement Rectification, Dismisses Late Application

Court Upholds Time Limit for Tax Settlement Rectification, Dismisses Late Application

This case involves Jay Kumar Singh (the petitioner) challenging an order by the Settlement Commission that dismissed his application for rectification of a tax settlement order. The application was rejected on the grounds of being filed after the statutory time limit. The High Court upheld the Settlement Commission's decision, dismissing the writ petition.

Get the full picture - access the original judgement of the court order here

Case Name:

Jay Kumar Singh Vs Principal Commissioner of Income Yax (Central Circle), Bhopal & Others (High Court of Madhya Pradesh)

Writ Petition No.12972 of 2018

Date: 6th January 2020

Key Takeaways:

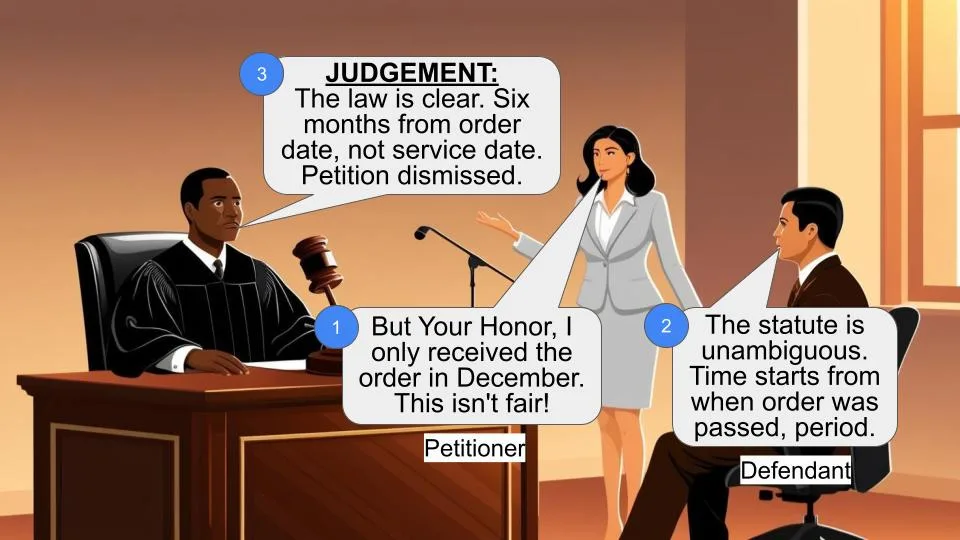

1. The court strictly interpreted the time limit for filing rectification applications under Section 245D(6B) (of Income Tax Act, 1961).

2. The limitation period starts from the date of the order, not from the date of its service to the applicant.

3. The court emphasized the legislature's right to impose reasonable conditions on statutory rights.

Issue:

Was the Settlement Commission correct in dismissing the petitioner's application for rectification of a tax settlement order on the grounds that it was filed after the statutory time limit?

Facts:

1. The petitioner filed an application for settlement under Section 245C (of Income Tax Act, 1961) on 24.02.2015 for the period 2007-08 to 2013-14.

2. The Settlement Commission passed an order under Section 245D(4) (of Income Tax Act, 1961) on 28.11.2016.

3. The petitioner claims the order was served to him in December 2016.

4. The petitioner filed an application for rectification under Section 245D(6B) (of Income Tax Act, 1961) on 30.06.2017.

5. The Settlement Commission dismissed this application as time-barred on 18.12.2017.

Arguments:

Petitioner's Arguments:

1. The limitation period should start from the date of service of the order, not the date of the order itself.

2. The application was filed within six months of the end of December 2016 when the order was served.

Revenue's Arguments:

1. The proviso to Section 245D(6B) (of Income Tax Act, 1961) creates a bar on entertaining rectification applications after six months from the end of the month in which the order was passed.

Key Legal Precedents:

1. AIR 1961 SC 1500 (Raja Harish Chandra Raj Singh vs. Deputy Land Acquisition Officer and another)

2. (2003) 6 SCC 186 (D. Saibaba vs. Bar Council of India and another)

3. (1959) 37 ITR 264 (Petlad Bulakhidas Mills Co. Ltd. vs. Raj Singh and another)

The court found these precedents distinguishable from the current case.

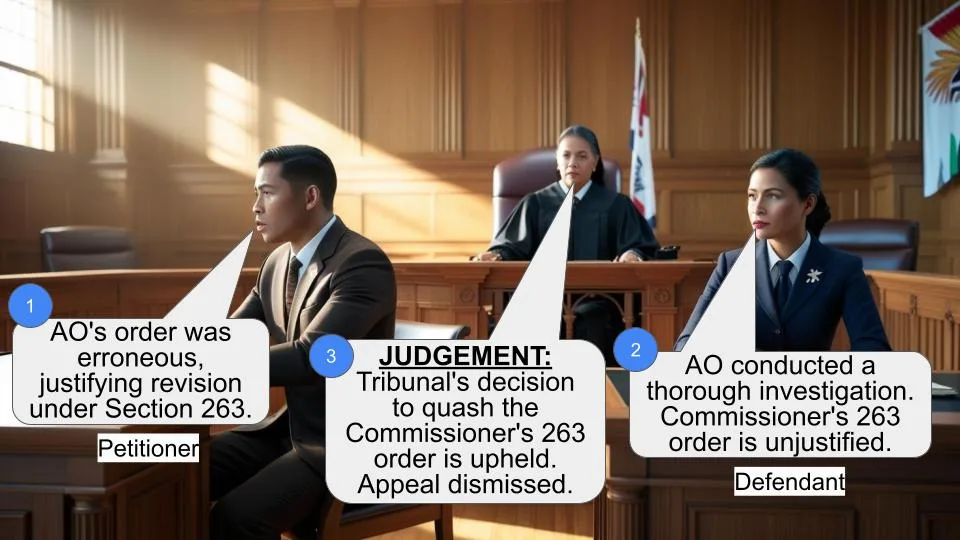

Judgement:

1. The court dismissed the writ petition, upholding the Settlement Commission's order.

2. It ruled that the six-month limitation period under Section 245D(6B) (of Income Tax Act, 1961) starts from the end of the month in which the order was passed, not from the date of service.

3. The court noted that even if the limitation started from the date of service, the petitioner failed to prove that the order was served on or after 30th December 2016.

4. The court emphasized the legislature's right to impose reasonable conditions on statutory rights.

FAQs:

Q1: Why did the court dismiss the petitioner's argument about the limitation period starting from the date of service?

A1: The court found that Section 245D(6B) (of Income Tax Act, 1961) clearly specifies the limitation period starts from the end of the month in which the order was passed, not from the date of service.

Q2: What is the significance of this judgment for future tax settlement cases?

A2: This judgment emphasizes strict adherence to statutory time limits in tax settlement cases, regardless of when the order is served to the parties.

Q3: Can the legislature impose time limits on statutory rights?

A3: Yes, the court affirmed that the legislature has the right to impose reasonable conditions, including time limits, on statutory rights it confers.

Q4: What should taxpayers keep in mind when dealing with Settlement Commission orders?

A4: Taxpayers should be aware of the strict six-month time limit for filing rectification applications, starting from the end of the month in which the order is passed, not from when they receive it.

Q5: How does this judgment impact the interpretation of similar provisions in other laws?

A5: While each law is unique, this judgment suggests courts may lean towards strict interpretation of statutory time limits unless the law explicitly provides for exceptions.

The petitioner by filing the instant writ petition under Article 226 of the Constitution of India has challenged an order dated 18.12.2017 (Annexure P-2) passed by the Settlement Commission whereby the application preferred by the petitioner under Section 245D(6B) (of Income Tax Act, 1961), 1961 (hereinafter referred to as “the Act”) for rectification of the order, has been dismissed.

2. The facts leading to the present petition are that the petitioner being an individual assessee filed an application under Section 245D(4) (of Income Tax Act, 1961) before the Settlement Commission for settlement on 24.2.2015 disclosing additional income as prescribed under Section 245C (of Income Tax Act, 1961) for the period 2007-08 to 2013-14. The said application was decided by the Settlement Commission vide order dated 28.11.2016. Noticing certain errors in the order dated 28.11.2016, the petitioner preferred an application (Annexure P-

1) under Section 245D(6B) (of Income Tax Act, 1961) for rectification of the mistakes on 30th June, 2017. The petitioner asserts that the order dated 28.11.2016 was served upon him in the month of December, 2016 and this averment was specifically made in the application so as to say that the application was within the period of limitation. However, the Settlement Commission vide order impugned herein has dismissed the application for rectification on the ground that the same is barred by limitation, which is challenged herein.

3. Learned counsel for the petitioner submitted that the order under Section 245C (of Income Tax Act, 1961) was passed on 28.11.2016 but it was served upon the petitioner in the month of December, 2016, hence, the limitation of six months as provided under Clause (a) of Section 245D(6B) (of Income Tax Act, 1961) read with the first proviso contained therein, would expire on 30.06.2017 and therefore, the application for rectification filed on 30.06.2017 was well within the limitation. Learned counsel has vehemently argued that for the purposes of Section 245D(6B) (of Income Tax Act, 1961), the limitation ought to have been counted from the date of service of the order and not from the date of the order itself. In this context, he has placed heavy reliance upon the two judgments of the Supreme Court reported in AIR 1961 SC 1500 (Raja Harish Chandra Raj Singh vs. Deputy Land Acquisition Officer and another) and (2003) 6 SCC 186 (D. Saibaba vs. Bar Council of India and another). Reliance has also been placed upon a Division Bench decision of Bombay High Court reported in (1959) 37 ITR 264 (Petlad Bulakhidas Mills Co. Ltd. vs. Raj Singh and another).

4. Shri Lal, learned counsel appearing for the Revenue, on the other

hand, arguing in support of the impugned order has contended that the proviso attached to Section 245D(6B) (of Income Tax Act, 1961) creates a bar in entertaining an application for rectification after the expiry of six months from the end of the month in which an order under sub-section (4) of Section 245D (of Income Tax Act, 1961) is passed by the Settlement Commission.

5. We have heard learned counsel for the parties and find that the present petition deserves to be dismissed.

6. Section 245D (of Income Tax Act, 1961) lays down procedure on receipt of an application under Section 245C (of Income Tax Act, 1961). Under sub-section (6B) thereof, the Settlement Commission has been empowered to rectify any mistake apparent from the record in the order passed by it under sub-section (4) thereof. Sub-section (6B) of Section 245D (of Income Tax Act, 1961) reads as under:-

“(6B) The Settlement Commission may, with a view to rectifying any mistake apparent from the record, amend any order passed by it under sub- section (4) –

(a) at any time within a period of six months from the end of the month in which the order was passed; or

(b) at any time within the period of six months from the end of the month in which an application for rectification has been made by the Principal Commissioner or the Commissioner or the applicant, as the case may be:

Provided that no application for rectification shall be made by the Principal Commissioner or the Commissioner or the applicant after the expiry of six months from the end of the month in which an order under sub-section (4) is passed by the Settlement Commission:

Provided further that an amendment which has the effect of modifying the liability of the applicant shall not be made under this sub- section unless the Settlement Commission has given notice to the applicant and the Principal Commissioner or Commissioner of its intention to do so and has allowed the applicant and the Principal Commissioner or Commissioner an opportunity of being heard.”

7. A perusal of sub-section (6B) of Section 245D (of Income Tax Act, 1961) makes it amply clear that any mistake apparent from the record in the order passed by the Settlement Commission under sub-section (4) of Section 245D (of Income Tax Act, 1961) may be rectified at any time within a period of six months from the end of the month in which the order was passed or at any time within a period of six months from the end of the month in which an application for rectification has been made by the Principal Commissioner or the Commissioner or the applicant, as the case may be. The first proviso to sub- section (6B) further creates an embargo for making any such application for rectification after the expiry of six months from the end of the month in which an order under sub-section (4) is passed by the Settlement Commission. In the present case, the order under sub-section (4) of Section 245D (of Income Tax Act, 1961) was passed by the Settlement Commission on 28.11.2016. Thus, six months from the end of the month in which the order was passed, expired on 31st May, 2017. Admittedly, the application under Section 245D(6B) (of Income Tax Act, 1961) was filed by the petitioner on 30.06.2017 which was barred by limitation as provided under sub-section (6B) thereof.

8. Still further, even if the argument advanced by the petitioner that the limitation of six months for entertaining application under Section 245D(6B) (of Income Tax Act, 1961) would start running from the date the order was served on the petitioner, is considered, there is nothing to show as to on which date in the month of December, 2016 the order was served upon the petitioner. The petitioner has only stated that the order dated 28.11.2016 was served upon him in the month of December, 2016 and has not demonstrated that the order dated 28.11.2016 was served upon him on or after 30th December, 2016 so as to claim that the application filed by the petitioner on 30th June, 2017 was within limitation. Thus, considering the controversy from this angle also, no case is made out in favour of the petitioner.

9. In Supreme Court decision in Raja Harish Chandra Raj Singh (supra), relied upon by the learned counsel for the petitioner, the question arose for consideration as to whether the application filed by the petitioner under Section 18 of the Land Acquisition Act, 1894 was in time or not. The proviso to Section 18 of the Income Tax Act, 1961 deals with the question of limitation.

The Supreme Court observed that Section 12(2) of the Income Tax Act, 1961 makes it obligatory on the Collector to give immediate notice of his award to such of the persons interested as are not present personally or by their representatives when the award is made. It is in this background, the Court held that the failure of the Collector to discharge his obligation under Section 12(2) of the Income Tax Act, 1961 would directly tend to make ineffective the right of the party to make an application under Section 18 (of Income Tax Act, 1961) and therefore, the High Court was in error in coming to the conclusion that the application made by the appellant in the said proceedings was barred under the proviso to Section 18 of the Income Tax Act, 1961. The relevant extract of the said decision reads as under:-

“7. In this connection it is material to recall the fact that under section 12(2) (of Income Tax Act, 1961) it is obligatory on the Collector to give immediate notice of the award to the persons interested as are not present personally or by their representatives when the award is made. This requirement itself postulates the necessity of the communication of the award to the party concerned.

The Legislature recognised that the making of the award under section 11 (of Income Tax Act, 1961) followed by its filing under Section 12(1) (of Income Tax Act, 1961) would not meet the requirements of justice before bringing the award into force. It thought that the communication of the award to the party concerned was also necessary, and so by the use of the mandatory words an obligation is placed on the Collector to communicate the award immediately to the person concerned. It is significant that the section requires the Collector to give notice of the award immediately after making it. This provision lends support to the view which we have taken about the construction of the expression "from the date of the Collector's award" in the proviso to Section 18 (of Income Tax Act, 1961). It is because communication of the order is regarded by the Legislature as necessary that Section 12(2) (of Income Tax Act, 1961) has imposed an obligation on the Collector and if the relevant clause in the proviso is read in the light of this statutory requirement it tends to show that the literal and mechanical construction of the said clause would be wholly inappropriate. It would indeed be a very curious result that the failure of the Collector to discharge his obligation under Section 12(2) (of Income Tax Act, 1961) should directly tend to make ineffective the right of the party to make an application under Section 18 (of Income Tax Act, 1961), and this result could not possibly have been intended by the legislature.”

However, in the present case, under sub-section (6B) of Section 245D (of Income Tax Act, 1961), there is no such requirement expressly provided for communication of the order of which rectification is sought, rather the said provision entitles both the Principal Commissioner or the Commissioner or the applicant to seek rectification of any mistake apparent from the record in the order passed by the Settlement Commission under sub-section (4) of Section 245D (of Income Tax Act, 1961) within six months from the end of the month when the order, rectification of which is sought, was passed. Thus, the decision in Raja Harish Chandra Raj Singh (supra) does not confer any advantage to the petitioner.

10. Similarly, another decision of the Supreme Court in D. Saibaba (supra) and Division Bench decision of Bombay High Court in Petlad Bulakhidas Mills (supra) relied upon by the learned counsel for the petitioner are also of no help to the petitioner being distinguishable on facts and passed in the cases considering different enactments. These decisions were also referred to by the petitioner before the learned Settlement Commission and the Commission observed as under:-

“5. After considering the arguments of both the sides and legal position on the issue, we are of the opinion that none of these case laws are directly on section 245D(6B) (of Income Tax Act, 1961) and to clarify the intent of legislature on the limitation period, a proviso to this section has been inserted w.e.f. 01.06.2015. This proviso clearly mentions that the time period of six months for filing rectification application is from date of passing the order u/s 245D(4) (of Income Tax Act, 1961) and not from its date of receipt by the PCIT or the applicant.

There is no dispute that application has been filed after six months from the end of the month of passing the order u/s 245D(4) (of Income Tax Act, 1961). Further, section 268 (of Income Tax Act, 1961) referred by the applicant relates to cases of exclusion of time for taking a copy of order where the order has not been served upon the applicant. In the present case the order has been served upon the applicant and the applicant has never asked for any copy of un-served order. We are of the opinion that the law is unambiguous in its intent and ample time of six months was available with the applicant to file the rectification application. As the present application has been filed beyond a period of end of six months from the end of month in which the order u/s 245D(4) (of Income Tax Act, 1961) was passed, we are inclined to reject the application of the applicant considering it to be non-est. Since, the application has been held to be non-est, the other substantive issues are not being adjudicated on merit.”

11. We do not find any error in the findings recorded by the learned Settlement Commission warranting interference in exercise of power of judicial review. That apart, if any right has been conferred by the Legislature, it equally has the right to take it away or prescribe reasonable conditions for the exercise of the right. The Legislature would be perfectly within its right to regulate any right conferred by it while imposing conditions or restrictions on its exercise.

12. In view of the foregoing reasons, the writ petition sans substance and is accordingly dismissed.

(Ajay Kumar Mittal) (Vijay Kumar Shukla)

Chief Justice Judge

×

Questions

Court Upholds Time Limit for Tax Settlement Rectification, Dismisses Late Application

Write your CommentSimilar Posts

Generic

- Reportdata/6150.pdf